Key takeaways

- The Hormuz blockade is exposing oil and LNG as structural security liabilities just as electrification and renewables have become economically competitive.

- Fossil‑fuel price shocks are accelerating the shift from direct fuel use to electricity, particularly in power generation and road transport.

- Countries with strong domestic renewable resources and robust grids are already demonstrating what ‘electricity‑first’ energy systems can look like.

- We believe asset allocators need to reweight energy allocations towards businesses positioned to benefit directly from rising electricity demand.

The world is reeling from what the IEA calls the worst energy shock on record [1] – a blockade through Hormuz that has choked off a quarter of global oil supply and significant volumes of liquefied natural gas (LNG).[2] Explosive price volatility, fuel rationing and demand-based restrictions evoke the systemic vulnerability felt after Fukushima, but this crisis is different in one critical respect. This time the world is ready to pivot at scale away from fossil fuels towards electrification more broadly, renewables and more secure, local power systems.

As these shockwaves spread, they are not just disrupting economic activity; they are accelerating a structural energy transition that was already underway. For investors, the implications of the seismic shifts that could follow a major energy disruption like this are critical – requiring a decisive reweighting of energy allocations towards electricity-focused assets.

Oil shocks in an electrification era

Fukushima dramatically changed how Japan and, by extension, parts of Europe thought about nuclear power and their mix of electricity supply options; today, the Hormuz crisis is prompting a similar reaction away from oil and LNG at the margin, and illustrating the extreme vulnerability of large-scale fossil fuel installations in that region.

The war in Ukraine was the first major warning for economies heavily dependent on imported Russian gas, exposing the vulnerability of supply‑concentrated systems. Policy responses at the time focused largely on diversifying gas suppliers and filling storage rather than structurally reshaping energy systems. A second large fossil‑fuel supply shock in four years now makes that incremental approach insufficient: reducing exposure to imported fuels and accelerating investment in renewables, storage and grids has become a policy necessity rather than a choice.

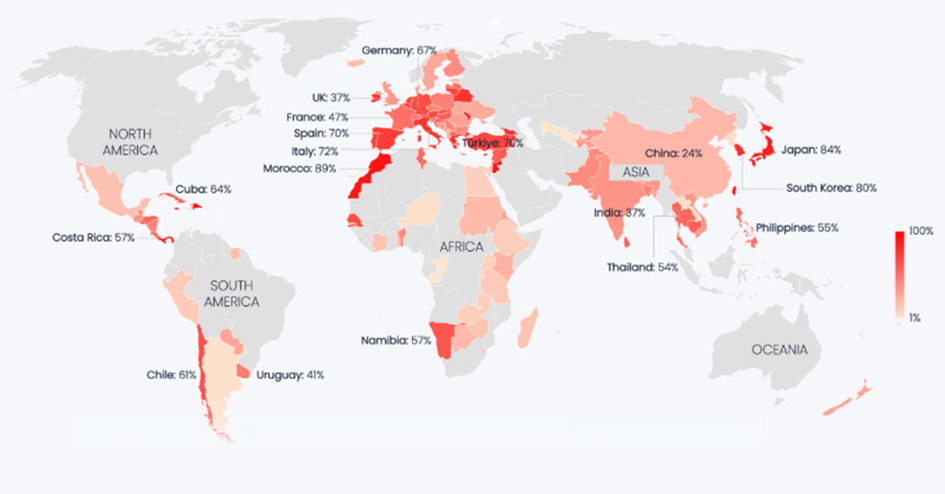

Chart 1 shows how widely exposed the world is: around three‑quarters of the global population live in countries that are net fossil‑fuel importers, with Asia and Europe among the most vulnerable.[3] Outside the United States – which has domestic oil and gas resources but remains exposed to higher global prices – most economies are now confronting the reality that shallow strategic reserves are insufficient and future energy shocks are a growing concern.

Chart 1 – Fossil fuel import dependency is widespread

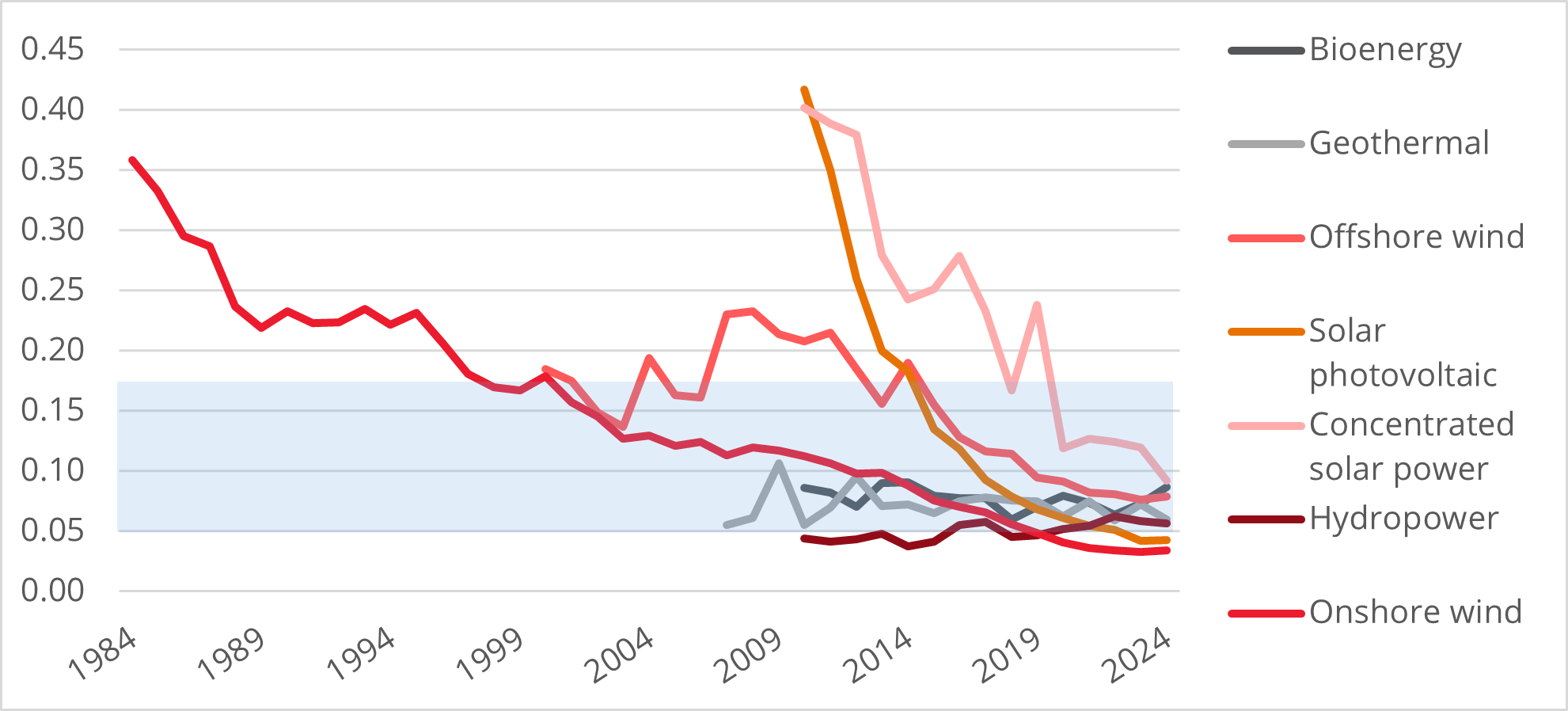

What makes this shock different from the oil crises of the 1970s is that it is landing on a system that is now technologically ready to substitute. In power, new renewables are now competitive or cheaper than new fossil capacity in most markets (Chart 2); in transport, electric vehicles (EVs) are approaching or have already reached cost parity with internal combustion engine (ICE) vehicles.[4] The security case to consume less oil and gas therefore now reinforces, rather than contradicts, the economic case.

Against that backdrop, we believe that many countries are likely to make reducing reliance on imported fossil fuels an explicit goal of energy policy – using higher strategic reserves, demand‑side measures and, above all, increased domestic investment in renewables, storage and grids.

The economics already flipped

Global levelised‑cost data show that the cost of electricity from new onshore wind and utility‑scale solar has fallen dramatically over the last decade and now typically sits below that of new coal and gas‑fired generation on a per‑kilowatt‑hour basis – see Chart 2. Higher and more volatile fossil‑fuel prices since the 2021–23 global energy crisis [5] have amplified this advantage, raising the effective hurdle rate for new fossil investment and making renewables look even more attractive than they already did on a pure cost basis. In effect, hydrocarbons now face a “two‑factor” risk: the usual price cycle plus the growing risk of physical disruption and security‑driven policy responses.

Chart 2 – Levelised cost of new wind/solar vs fossil fuels (USD)

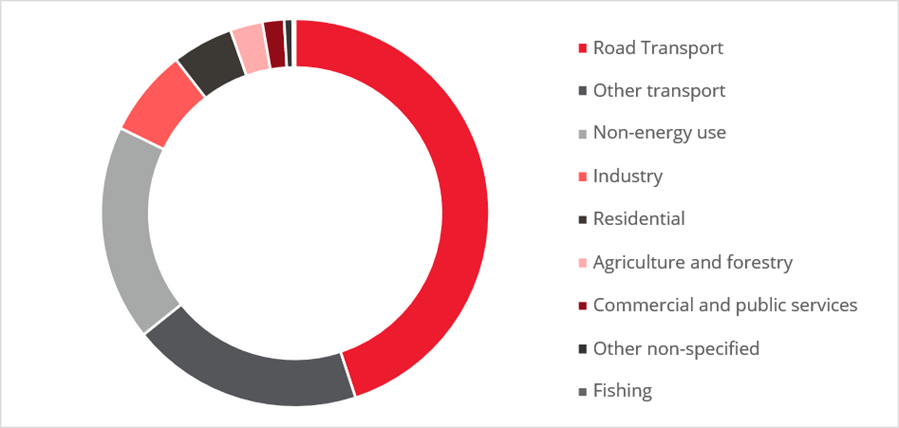

Sector data from the IEA show that road transport remains the single largest source of final oil demand globally, followed by petrochemicals, aviation and shipping. That concentration means that accelerating EV adoption and improving efficiency in vehicles could have a disproportionate impact on long-term oil consumption, even if other uses of oil prove harder to displace.

Chart 3: Global oil consumption by sector (%)

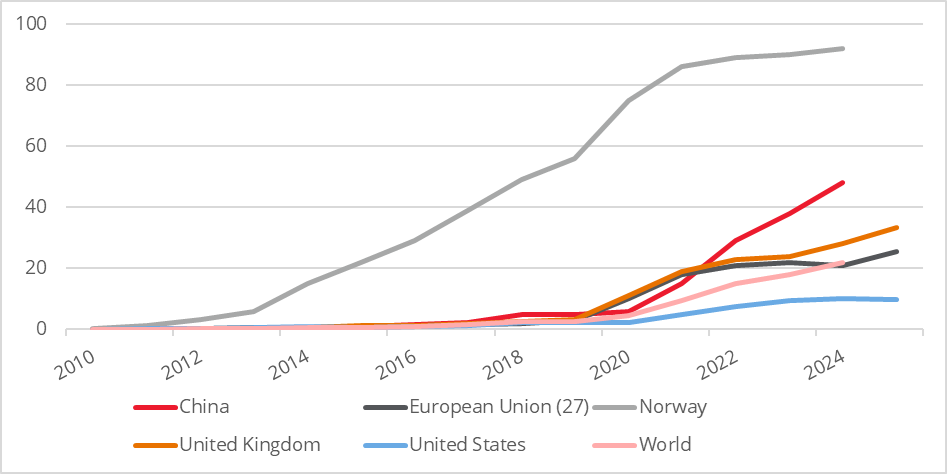

EV market share of new car sales has risen sharply over the past few years, with many markets in Europe and China already seeing double‑digit penetration and rapid growth in Asia and Latin America from a lower base.[6] As battery prices have fallen and driving ranges per charge increased, the total cost of ownership for EVs has converged with ICE vehicles in a growing number of segments, especially where fuel is taxed or imported.[7] That makes higher oil prices – and the risk that they remain elevated – an additional tailwind for EV adoption.

Chart 4 – EV share of new car sales (%)

Concerns that shifting from Middle Eastern fuels to Asian‑manufactured solar modules, batteries or Danish wind components simply swaps one form of dependence for another are understandable but often overstated. Once built, solar and wind assets are powered by local resources; they do not depend on continuous fuel deliveries that can be interrupted or repriced overnight. Hardware typically accounts for a minority of lifetime project costs, with the bulk tied up in financing, labour, land and grid connections; and the equipment itself is geographically diversified. Many parts of the world are also decentralizing manufacturing and assembly of renewable systems, so we expect further diversification of these concerns. Indeed, Tesla has announced plans to develop as much as 100GW of solar manufacturing capacity in the US recently.[8]

Natural gas: A transition resource for power systems

Oil has been phased out of most electricity supply systems globally, but LNG has grown rapidly as an alternative to both oil and coal. Gas still plays an important role in electricity supply systems. However, the rapid advancement of battery storage – both in technical terms, as well as a rapid decline in cost of electricity (LCOE) – means the need for firm or baseload power supply provided by LNG is actually starting to decline, and could decline by more than 90%, in our view. This reality is so new that many market experts openly deny this possibility. AI‑driven data‑centre demand in the US complicates this picture, but we believe this will not change the basic direction of travel for fossil fuel demand.

Different paths to electrification: Asia, China and Europe

Electrification is not unfolding in the same way everywhere. Asia ex‑China is experiencing the Hormuz shock most acutely because of its high import dependence and shallow reserves; here, the immediate policy levers include accelerating EV uptake to cut oil demand, ramping renewables to reduce LNG or piped gas needs, and reinforcing grids to absorb more variable generation. China, by contrast, enters this crisis with a huge installed base of coal and increasing nuclear and renewable capacity that limits exposure to seaborne imports of fossil fuels.

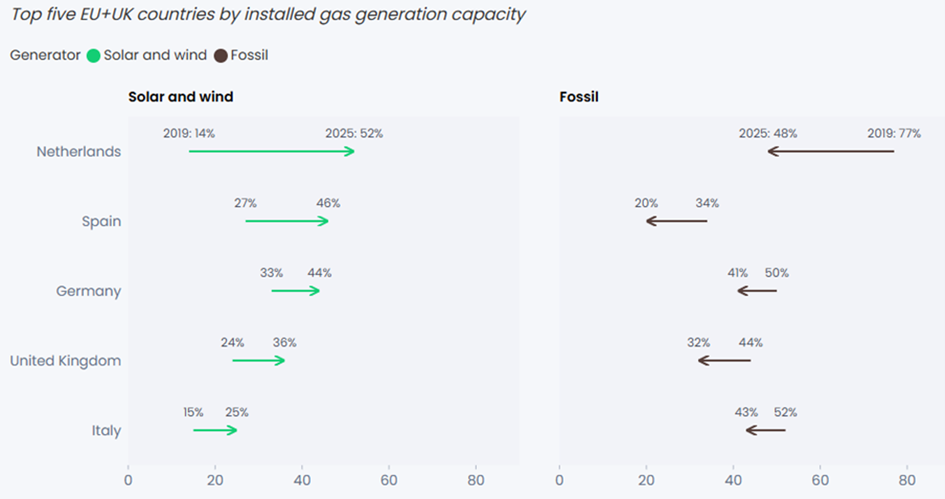

In Europe, the picture is different again. Spain, in particular, offers a striking example of what an electricity‑first system can look like in a developed market. Over the past decade it has delivered rapid growth in wind and solar, while bringing down the share of fossil‑fired generation and weakening the link between gas prices and power prices. Crucially, this has been driven largely by the economic merit of renewables – supported by hydro and interconnection – rather than by policy: even as political sentiment has oscillated, renewables have remained the cheapest way to add capacity.[9]

Chart 5 – Wind and solar share of electricity generation, EU and UK, H1 2019–H1 2025

Taken together, these regional stories reinforce a common message: the transition away from fuel and towards power is already under way globally, but it is expressing itself differently depending on resource endowments, policy priorities and starting points.

Where does capital need to go?

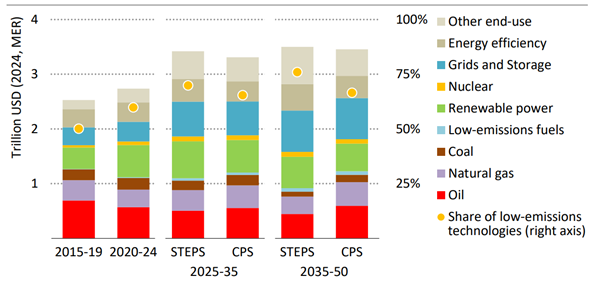

EVs, batteries, grids and firm low‑carbon generation are the enabling assets that turn higher electricity share into energy security, by shifting demand away from imported fuel and anchoring it in domestic, 24/7 power. IEA analysis shows that, under both the conservative Current Policies Scenario (CPS) and the Stated Policies Scenario (STEPS), global energy investment – including grids – needs to rise materially over the coming decades, with grid and storage investment playing a central role.

Chart 6 – Projected global energy and grid investment, CPS vs STEPS scenarios

For investors, the key building blocks of an electricity‑first energy system include:

- Local and domestic power generation: Renewables and, in some markets, nuclear are the technologies that convert domestic resources into electricity, reducing exposure to imported fuels while benefiting from improving economics.

- EVs as the visible edge of electrification: EVs translate high‑level system change into tangible consumer behaviour, directly displacing oil demand in transport and boosting electricity demand in a way that can be planned for.

- Batteries and flexibility: Storage and demand‑side response turn variable renewables into firm capacity by shifting energy across time, allowing grids to meet peak demand without relying on expensive fossil peakers.[10]

- Nuclear as firm low‑carbon capacity: Where social licence and regulatory frameworks permit, life extensions of existing nuclear fleets and, potentially, small modular reactors provide non‑fossil, on-demand power that reduces reliance on gas and oil in the broader power mix.

Much of this investment will be executed by listed renewables platforms, integrated utilities and regulated network operators, many of which currently trade at valuations that reflect their rate sensitivity more than their structural role in the new energy order. That creates a disconnect between fundamentals and market pricing that long‑term investors can exploit.

Rethinking energy exposures

Many asset allocators with energy exposure are still primarily exposed to oil and gas exploration and production, with little or no explicit allocation to electricity infrastructure. That may have made sense in a world where energy security meant securing fossil fuel flows. In a world that is being driven, by both economics and geopolitics, from fossil fuel direct use to power systems, investors risk becoming structurally underweight the very assets that stand to benefit from the new regime.

We believe ‘electricity companies’ – integrated utilities, renewables platforms, regulated grids and selected storage and flexibility assets – should increasingly sit at the core of an energy allocation. These are the businesses that build, own and operate the assets that generate, move and store power, that will gain share as fuel loses it, and that stand to benefit from a structurally higher security premium on fossil fuels. In our view, that makes today an attractive entry point to tilt existing energy allocations towards market share-winning electricity.

After Hormuz, there’s no going back

The Hormuz crisis has exposed oil and LNG as structural security liabilities just as electrification has become economically compelling. In much the same way that Fukushima locked in a multi‑decade reshaping of gas and power markets in Japan and Australia, today’s crisis is likely to lock in a protracted investment cycle in electricity infrastructure.

For policymakers, that means building electricity‑first systems – renewables, grids, storage and firm low‑carbon generation – that can shelter their economies from oil and gas disruption. For investors, it means ensuring that energy allocations are anchored in the parts of the system where security, economics and the transition all now point in the same direction – and where, in our view, the next decade of energy returns are most likely to be made.

Key Information

No investment strategy or risk management technique can guarantee returns or eliminate risks in any market environment. Past performance is not a guide to the future. The prices of investments and income from them may fall as well as rise and investors may not get back the full amount invested. Forecasts and estimates are based upon subjective assumptions about circumstances and events that may not yet have taken place and may never do so. The statements and opinions expressed in this article are those of the author as of the date of publication, and do not necessarily represent the view of Redwheel. This article does not constitute investment advice and the information shown is for illustrative purposes only.

References

[1] Oilprice.com

[2] UNCTAD

[4] IEA.org

[5] IEA.org

[6] Ember Energy, The EV leapfrog – how emerging markets are driving a global EV boom, December 2025

[7] IEA.org

[8] Bloomberg, March 2026

[9] IRENA.org – 91% of New Renewable Projects Now Cheaper Than Fossil Fuels Alternatives