We use strictly necessary cookies to enable our site to work and performance cookies to improve the visitor experience when visiting the site. We will only set performance cookies if you permit us to.

For more detailed information about the cookies we use, see the “Cookie Usage” section of our Privacy Policy

Convertible bonds provide a hybrid solution for investors looking for a balanced exposure to financial markets that combines the attractive elements of both equities and bonds. For more than a decade, our team has been deploying its proprietary models and systems to help identify the most attractive opportunities within the asset class. We provide a range of actively managed solutions, designed to exploit the attractive asymmetric return profile of convertible bonds with varying degrees of risk tolerance.

Emerging and frontier markets represent the fastest growing economies in the world. We believe the continued growth of these markets presents compelling opportunities across a range of industries. Our index agnostic, opportunistic approach has been honed for more than two decades, and the depth of experience garnered within our team allows us to participate in attractive growth opportunities that are off the beaten track for most investors.

We invest in a small number of high-quality European companies, where we identify potentially significant opportunities to create additional value by addressing certain company-specific issues. We then act as a catalyst for change by constructively working together with the companies and other shareholders.

A highly experienced team with an established track record of delivering positive outcomes for investors. Harnessing the full power of dividends is a tried and tested method of investing, with the potential to deliver value added long-term returns and lower-than-average volatility. The team looks for the rare combination of a premium yield, sustainable dividend and attractive valuation, which only occurs when controversy appears. By working hard to understand the nature of a controversy, we aim to lean the probability of investment success in your favour.

Japan is the world’s third largest economy and its corporate landscape is undergoing dramatic change. Through our joint venture with Tokyo-based Nissay Asset Management (NAM), we invest in a small number of select Japanese companies that are not valued to their full potential due to factors we see as rectifiable. We then engage in order to act as an agent for the change required to unlock value.

Sustainability, in its broadest context, is structurally changing the investment landscape from both a risk and opportunities perspective. The Redwheel Sustainable Growth team seeks to identify structural longer-term themes and dynamics in the economy and society. The team invests capital to take advantage of the potential return opportunities these themes and dynamics offer, and to facilitate and further advance the positive impact of investee companies on critical sustainability challenges and development goals.

We are long-term value investors who believe that short-term factors prompt many market participants to overreact to news which may have little or no impact on the true value of a company. This causes share prices to diverge from the intrinsic value of the underlying business and provides an opportunity for long-term investors to purchase shares at an attractive discount. This builds in a margin of safety but also provides meaningful long-term total return potential through both dividend income and capital appreciation.

Redwheel is committed to facilitating and delivering responsible investment in practice. In line with their investment freedoms, each investment team is responsible for the integration of sustainability considerations within their respective investment processes, consistent with firm-level policies.

Redwheel’s stewardship function focuses primarily on overseeing and supporting the stewardship activities of our investment teams, co-ordinating our involvement in external stewardship initiatives, and leading in the development of the stewardship that Redwheel does as a corporate entity.

What is Sustainability Strategy, Governance & Policy? Sustainability Strategy, Governance and Policy focuses in three areas.

Greenwheel is the sustainability insights partner to Redwheel’s Sustainable, Transition and Enhanced Integration funds. Greenwheel provides tailored thematic and sector level sustainability research and advice to fund managers, commissioned by fund managers.

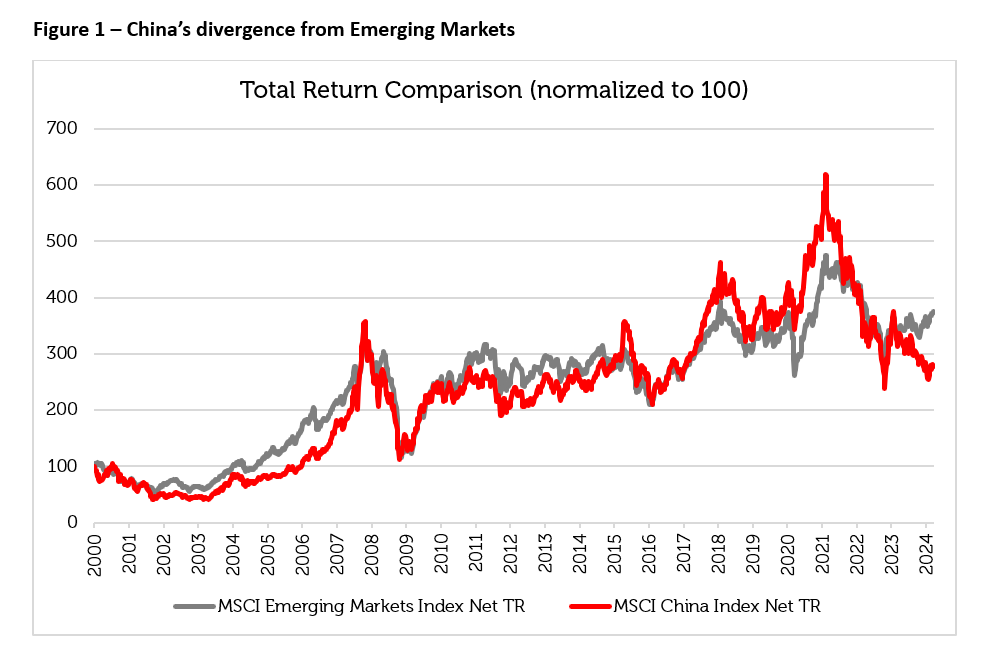

It seems that many investors have almost forgotten about China’s five-year bull run from February 2016 to February 2021, when the MSCI China Index gained over 100% in dollars, at a compound growth rate of over 15% per annum. The MSCI China technology sector posted even more impressive gains of over 30% per annum over the same period.

Since 2021, however, emerging markets in general – and China in particular – have been in the grip of a bear market. The reasons for the decline include the gradual withdrawal of fiscal stimulus and tightening of global monetary policy since the COVID-19 pandemic. China has also suffered from some of its own unique difficulties.

Causes of the bear market

Externally, the United States has imposed trade tariffs and technology restrictions that have curbed trade with China and reduced direct investment from the west. Domestically, China has imposed a variety of regulations on e-commerce, education, entertainment, finance and gaming companies with the aim of sharing wealth more equally between customers, shareholders and suppliers. These measures have hurt profitability for many listed companies. The drive to reduce dependence on debt in the property sector has reduced liquidity and slowed the growth in a key area of the Chinese economy. The decline in the rate of growth and profitability over the past three years has contributed to an equity bear market.

Source: Bloomberg, Redwheel as of 31 March 2024. The information shown above is for illustrative purposes. Past performance is not a guide to future results.

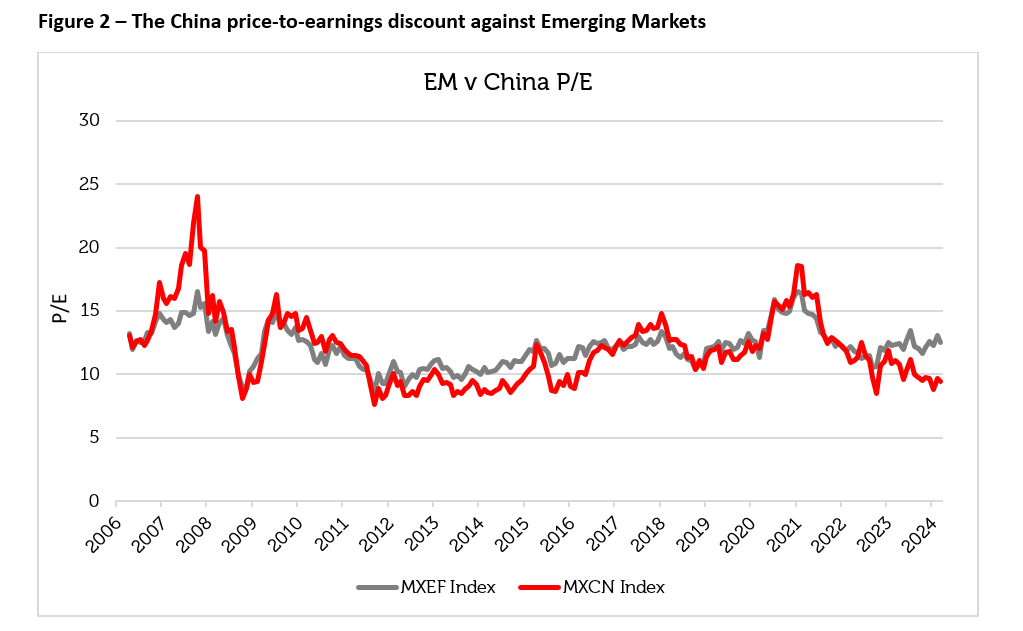

Depressed valuations

The fall in share prices since early 2021 means that MSCI China’s equity index is now attractively valued in both relative and absolute terms, in our view. From trading at a premium P/E ratio of over 20 in 2007, Chinese equities are now at a discount to the rest of EM with a valuation below 10 times forward earnings, close to the trough valuations of 2011 – 2015 from which the market subsequently recovered.

Source: Bloomberg, Redwheel as of 31 March 2024. The information shown above is for illustrative purposes. Past performance is not a guide to future results. No investment strategy or risk management technique can guarantee returns or eliminate risks in any market environment.

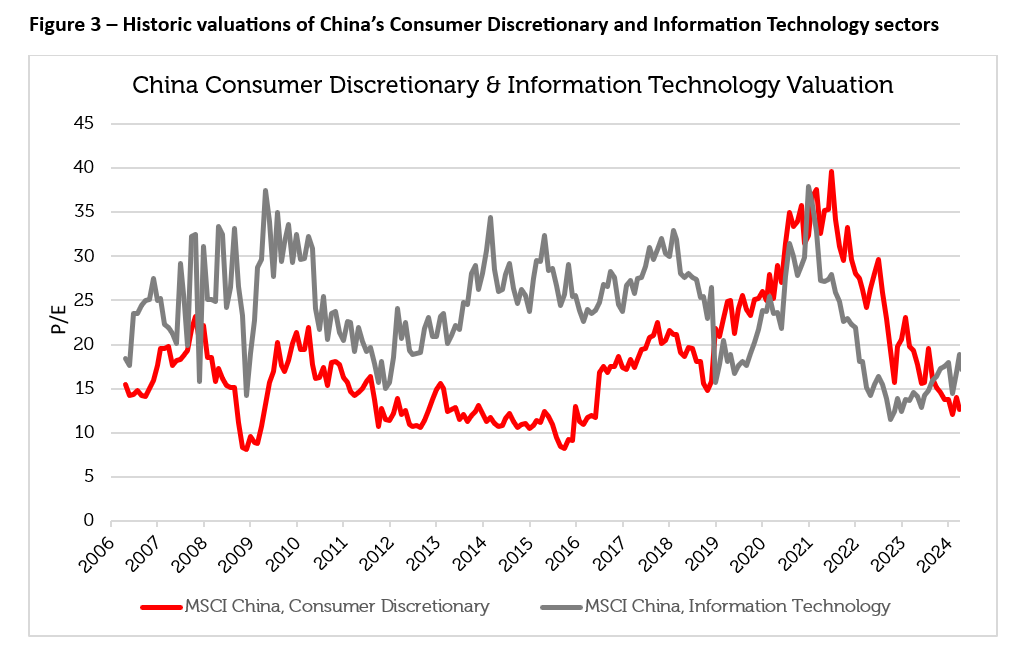

The Chinese equity market now has many attractively valued industry sectors. The Energy, Financial, Industrial and Real Estate sectors all trade on single-digit P/E multiples, with Real Estate and Financials showing dividend yields in the range of 7% – 8% (source: Bloomberg, Redwheel). High quality growth companies in the Consumer Discretionary and Technology sectors have on average experienced a halving of their valuations to levels seen only in periods of crisis, such as the Global Financial Crisis of 2008. Valuations have historically rebounded from these depressed levels.

Source: Bloomberg, Redwheel as of 31 March 2024. The information shown above is for illustrative purposes. Past performance is not a guide to future results.

China’s economic recovery and transformation

The Chinese equity market now requires patience for low valuations to result in better long run returns. The catalyst for the recovery might be new policy stimulus that the Chinese government has typically turned to during economic and financial downturns. First, on the monetary side, the People’s Bank of China has gradually reduced reserve requirements and interest rates to support aggregate demand. Second, specific actions have been designed to support the property market, including a reduction in down-payments, lowering mortgage rates and providing liquidity support to debt-constrained property developers. Third, the Chinese government explicitly wishes to boost domestic consumption in order to reduce reliance on exports and property development as the engines of growth. Policies were announced at the National People’s Congress (NPC) in March 2024 to promote higher sales of consumer durables, including the provision of credit, subsidies and trade-ins for automobiles and domestic appliances.

In the medium term, one of China’s goals is to redirect economic development towards the higher value-added manufacturing and technology sectors including electric vehicles, renewable energy production, smart appliances and services. The aim is to move away from fabricating low margin commodity products that China has relied on since joining the WTO in 2001, and towards a skills-based economy like Germany, which would raise both living standards and corporate profitability.

The successful implementation of short-term financial and monetary stimulus, together with long -term economic reform, would likely help China to narrow the current 30% valuation gap with the rest of Asia. Even now, we see Chinese companies demonstrating better profitability than the rest of the region. To illustrate, the MSCI China Index shows a higher Return on Equity (ROE) than the MSCI Asia ex-Japan Index, yet trades at a 30% P/E discount to the Asian index (Source: Bloomberg, Redwheel 26 April). In our view, economic renewal and stimulus should allow the equity market to re-rate as it has done from these levels in the past.

Key Information

No investment strategy or risk management technique can guarantee returns or eliminate risks in any market environment. Past performance is not a guide to future results. The prices of investments and income from them may fall as well as rise and an investor’s investment is subject to potential loss, in whole or in part. Forecasts and estimates are based upon subjective assumptions about circumstances and events that may not yet have taken place and may never do so. The statements and opinions expressed in this article are those of the author as of the date of publication, and do not necessarily represent the view of Redwheel. This article does not constitute investment advice and the information shown is for illustrative purposes only.

The Redwheel Emerging and Frontier Markets team explores the concentration challenge facing investors today and maps out under‑owned countries, sectors and themes that the team believes offer a richer blend of structural growth and genuine diversification.

Shaul Rosten, Analyst with the Redwheel Value and Income team looks at the striking similarities between today’s market exuberance and the dotcom era, highlighting stretched valuations, record IPO activity and the dominance of the technology sector.

As England’s World Cup campaign unfolds, the tournament provides a vivid reminder that sensible bets are grounded in probabilities. Supporters know that backing long-shot teams is unlikely to be rewarded, while favouring stronger sides with clear track records is more prudent. In his latest blog, Shaul Rosten of Redwheel's Value & Income team examines how value investing adopts a similar stance, focusing on quality businesses at attractive valuations, rather than richly priced growth narratives with low odds of delivery.

Redwheel ® and Ecofin ® are registered trademarks of RWC Partners Limited (“RWC”). The term “Redwheel” may include any one or more Redwheel branded regulated entities including RWC Asset Management LLP, which is authorised and regulated by the UK Financial Conduct Authority and the US Securities and Exchange Commission (“SEC”); RWC Asset Advisors (US) LLC, which is registered with the SEC; RWC Singapore (Pte) Limited, which is licensed as a Licensed Fund Management Company by the Monetary Authority of Singapore; Redwheel Australia Pty Ltd is an Australian Financial Services Licensee with the Australian Securities and Investment Commission; and Redwheel Europe Fondsmæglerselskab A/S which is regulated by the Danish Financial Supervisory Authority.

Redwheel may act as investment manager or adviser, or otherwise provide services, to more than one product pursuing a similar investment strategy or focus to the product detailed in this document. Redwheel and RWC (together “Redwheel Group”) seeks to minimise any conflicts of interest, and endeavours to act at all times in accordance with its legal and regulatory obligations as well as its own policies and codes of conduct.

This document is directed only at professional, institutional, wholesale or qualified investors. The services provided by Redwheel are available only to such persons. It is not intended for distribution to and should not be relied on by any person who would qualify as a retail or individual investor in any jurisdiction or for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to local law or regulation.

This document has been prepared for general information purposes only and has not been delivered for registration in any jurisdiction nor has its content been reviewed or approved by any regulatory authority in any jurisdiction.

The information contained herein does not constitute: (i) a binding legal agreement; (ii) legal, regulatory, tax, accounting or other advice; (iii) an offer, recommendation or solicitation to buy or sell shares in any fund, security, commodity, financial instrument or derivative linked to, or otherwise included in a portfolio managed or advised by Redwheel; or (iv) an offer to enter into any other transaction whatsoever (each a “Transaction”). Redwheel Group bears no responsibility for your investment research and/or investment decisions and you should consult your own lawyer, accountant, tax adviser or other professional adviser before entering into any Transaction. No representations and/or warranties are made that the information contained herein is either up to date and/or accurate and is not intended to be used or relied upon by any counterparty, investor or any other third party.

Redwheel Group uses information from third party vendors, such as statistical and other data, that it believes to be reliable. However, the accuracy of this data, which may be used to calculate results or otherwise compile data that finds its way over time into Redwheel Group research data stored on its systems, is not guaranteed. If such information is not accurate, some of the conclusions reached or statements made may be adversely affected. Any opinion expressed herein, which may be subjective in nature, may not be shared by all directors, officers, employees, or representatives of Group and may be subject to change without notice. Redwheel Group is not liable for any decisions made or actions or inactions taken by you or others based on the contents of this document and neither Redwheel Group nor any of its directors, officers, employees, or representatives (including affiliates) accepts any liability whatsoever for any errors and/or omissions or for any direct, indirect, special, incidental, or consequential loss, damages, or expenses of any kind howsoever arising from the use of, or reliance on, any information contained herein.

Information contained in this document should not be viewed as indicative of future results. Past performance of any Transaction is not indicative of future results. The value of investments can go down as well as up. Certain assumptions and forward looking statements may have been made either for modelling purposes, to simplify the presentation and/or calculation of any projections or estimates contained herein and Redwheel Group does not represent that that any such assumptions or statements will reflect actual future events or that all assumptions have been considered or stated. There can be no assurance that estimated returns or projections will be realised or that actual returns or performance results will not materially differ from those estimated herein. Some of the information contained in this document may be aggregated data of Transactions executed by Redwheel that has been compiled so as not to identify the underlying Transactions of any particular customer.

No representations or warranties of any kind are intended or should be inferred with respect to the economic return from, or the tax consequences of, an investment in a Redwheel-managed fund.

This document expresses no views as to the suitability or appropriateness of the fund or any other investments described herein to the individual circumstances of any recipient.

The information transmitted is intended only for the person or entity to which it has been given and may contain confidential and/or privileged material. In accepting receipt of the information transmitted you agree that you and/or your affiliates, partners, directors, officers and employees, as applicable, will keep all information strictly confidential. Any review, retransmission, dissemination or other use of, or taking of any action in reliance upon, this information is prohibited. Any distribution or reproduction of this document is not authorised and is prohibited without the express written consent of Redwheel Group.

Funds managed by Redwheel are not, and will not be, registered under the Securities Act of 1933 (the “Securities Act”) and are not available for purchase by US persons (as defined in Regulation S under the Securities Act) except to persons who are “qualified purchasers” (as defined in the Investment Company Act of 1940) and “accredited investors” (as defined in Rule 501(a) under the Securities Act).

This document does not constitute an offer to sell, purchase, subscribe for or otherwise invest in units or shares of any fund managed by Redwheel. Any offering is made only pursuant to the relevant offering document and the relevant subscription application. Prospective investors should review the offering memorandum in its entirety, including the risk factors in the offering memorandum, before making a decision to invest.

AIFMD and Distribution in the European Economic Area (“EEA”)

The Alternative Fund Managers Directive (Directive 2011/61/EU) (“AIFMD”) is a regulatory regime which came into full effect in the EEA on 22 July 2014. RWC Asset Management LLP is an Alternative Investment Fund Manager (an “AIFM”) to certain funds managed by it (each an “AIF”). The AIFM is required to make available to investors certain prescribed information prior to their investment in an AIF. The majority of the prescribed information is contained in the latest Offering Document of the AIF. The remainder of the prescribed information is contained in the relevant AIF’s annual report and accounts. All of the information is provided in accordance with the AIFMD.

In relation to each member state of the EEA (each a “Member State”), this document may only be distributed and shares in a Redwheel fund (“Shares”) may only be offered and placed to the extent that (a) the relevant Redwheel fund is permitted to be marketed to professional investors in accordance with the AIFMD (as implemented into the local law/regulation of the relevant Member State); or (b) this document may otherwise be lawfully distributed and the Shares may lawfully be offered or placed in that Member State (including at the initiative of the investor).

Information Required for Offering in Switzerland of Foreign Collective Investment Schemes to Qualified Investors within the meaning of Article 10 CISA.

This is an advertising document.

The representative and paying agent of the Redwheel-managed funds in Switzerland (the “Representative in Switzerland”) FIRST INDEPENDENT FUND SERVICES LTD, Feldeggstrasse 12, CH-8008 Zurich. Swiss Paying Agent: Helvetische Bank AG, Seefeldstrasse 215, CH-8008 Zurich. In respect of the units of the Redwheel-managed funds offered in Switzerland, the place of performance is at the registered office of the Swiss Representative. The place of jurisdiction is at the registered office of the Swiss Representative or at the registered office or place of residence of the investor.

Redwheel ® and Ecofin ® are registered trademarks of RWC Partners Limited. The term “Redwheel” may include any one or more Redwheel regulated entities including RWC Asset Management LLP, which is authorised and regulated by the Financial Conduct Authority in the United Kingdom (“RWC”). RWC is incorporated in England and Wales with its registered office at Verde 4th Floor, 10 Bressenden Place, London, SW1E 5DH, United Kingdom and its registered number is OC332015.

No investment strategy or risk management technique can guarantee returns or eliminate risks in any market environment.The term “RWC” may include any one or more RWC branded entities including RWC Partners Limited and RWC Asset Management LLP, each of which is authorised and regulated by the UK Financial Conduct Authority and, in the case of RWC Asset Management LLP, the US Securities and Exchange Commission; RWC Asset Advisors (US) LLC, which is registered with the US Securities and Exchange Commission; and RWC Singapore (Pte) Limited, which is licensed as a Licensed Fund Management Company by the Monetary Authority of Singapore.RWC may act as investment manager or adviser, or otherwise provide services, to more than one product pursuing a similar investment strategy or focus to the product detailed in this audio. RWC seeks to minimise any conflicts of interest, and endeavours to act at all times in accordance with its legal and regulatory obligations as well as its own policies and codes of conduct.This audio is directed only at professional, institutional, wholesale or qualified investors. The services provided by RWC are available only to such persons. It is not intended for distribution to and should not be relied on by any person who would qualify as a retail or individual investor in any jurisdiction or for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to local law or regulation.This audio has been prepared for general information purposes only and has not been delivered for registration in any jurisdiction nor has its content been reviewed or approved by any regulatory authority in any jurisdiction. The information contained herein does not constitute: (i) a binding legal agreement; (ii) legal, regulatory, tax, accounting or other advice; (iii) an offer, recommendation or solicitation to buy or sell shares in any fund, security, commodity, financial instrument or derivative linked to, or otherwise included in a portfolio managed or advised by RWC; or(iv) an offer to enter into any other transaction whatsoever (each a “Transaction”). No representations and/or warranties are made that the information contained herein is either up to date and/or accurate and is not intended to be used or relied upon by any counterparty, investor or any other third party.RWC uses information from third party vendors, such as statistical and other data, that it believes to be reliable. However, the accuracy of this data, which may be used to calculate results or otherwise compile data that finds its way over time into RWC research data stored on its systems, is not guaranteed. If such information is not accurate, some of the conclusions reached or statements made may be adversely affected. RWC bears no responsibility for your investment research and/or investment decisions and you should consult your own lawyer, accountant, tax adviser or other professional adviser before entering into any Transaction. Any opinion expressed herein, which may be subjective in nature, may not be shared by all directors, officers, employees, or representatives of RWC and may be subject to change without notice. RWC is not liable for any decisions made or actions or in actions taken by you or others based on the contents of this audio and neither RWC nor any of its directors, officers, employees, or representatives (including affiliates) accepts any liability whatsoever for any errors and/or omissions or for any direct, indirect, special, incidental, or consequential loss, damages, or expenses of any kind howsoever arising from the use of, or reliance on, any information contained herein.Information contained in this audio should not be viewed as indicative of future results. Past performance of any Transaction is not indicative of future results. The value of investments can go down as well as up. Certain assumptions and forward looking statements may have been made either for modelling purposes, to simplify the audio and/or calculation of any projections or estimates contained herein and RWC does not represent that that any such assumptions or statements will reflect actual future events or that all assumptions have been considered or stated. Forward-looking statements are inherently uncertain, and changing factors such as those affecting the markets generally, or those affecting particular industries or issuers, may cause results to differ from those discussed. Accordingly, there can be no assurance that estimated returns or projections will be realised or that actual returns or performance results will not materially differ from those estimated herein. Some of the information contained in this audio may be aggregated data of Transactions executed by RWC that has been compiled so as not to identify the underlying Transactions of any particular customer.The information transmitted is intended only for the person or entity to which it has been given and may contain confidential and/or privileged material. In accepting receipt of the information transmitted you agree that you and/or your affiliates, partners, directors, officers and employees, as applicable, will keep all information strictly confidential. Any review, retransmission, dissemination or other use of, or taking of any action in reliance upon, this information is prohibited. The information contained herein is confidential and is intended for the exclusive use of the intended recipient(s) to which this audio has been provided. Any distribution or reproduction of this audio is not authorised and is prohibited without the express written consent of RWC or any of its affiliates.Changes in rates of exchange may cause the value of such investments to fluctuate. An investor may not be able to get back the amount invested and the loss on realisation may be very high and could result in a substantial or complete loss of the investment. In addition, an investor who realises their investment in a RWC-managed fund after a short period may not realise the amount originally invested as a result of charges made on the issue and/or redemption of such investment. The value of such interests for the purposes of purchases may differ from their value for the purpose of redemptions. No representations or warranties of any kind are intended or should be inferred with respect to the economic return from, or the tax consequences of, an investment in a RWC-managed fund. Current tax levels and reliefs may change. Depending on individual circumstances, this may affect investment returns. Nothing in this document constitutes advice on the merits of buying or selling a particular investment. This audio expresses no views as to the suitability or appropriateness of the fund or any other investments described herein to the individual circumstances of any recipient.AIFMD and Distribution in the European Economic Area (“EEA”)The Alternative Fund Managers Directive (Directive 2011/61/EU)(“AIFMD”) is a regulatory regime which came into full effect in the EEA on 22 July 2014. RWC Asset Management LLP is an Alternative Investment Fund Manager (an “AIFM”) to certain funds managed by it (each an “AIF”). The AIFM is required to make available to investors certain prescribed information prior to their investment in an AIF. The majority of the prescribed information is contained in the latest Offering Document of the AIF. The remainder of the prescribed information is contained in the relevant AIF’s annual report and accounts. All of the information is provided in accordance with the AIFMD.In relation to each member state of the EEA (each a “Member State”),this document may only be distributed and shares in a RWC fund(“Shares”) may only be offered and placed to the extent that (a) the relevant RWC fund is permitted to be marketed to professional investors in accordance with the AIFMD (as implemented into the local law/regulation of the relevant Member State); or (b) this audio may otherwise be lawfully distributed and the Shares may lawfully offered or placed in that Member State (including at the initiative of the investor).Information Required for Distribution of Foreign Collective Investment Schemes to Qualified Investors in SwitzerlandThe representative and paying agent of the RWC-managed funds in Switzerland (the “Representative in Switzerland”) FIRST INDEPENDENT FUND SERVICES LTD, Klausstrasse 33, CH-8008 Zurich. Swiss Paying Agent: Helvetische Bank AG, Seefeldstrasse 215, CH-8008 Zurich. In respect of the units of the RWC-managed funds distributed in Switzerland, the place of performance and jurisdiction is at the registered office of the Representative in Switzerland.