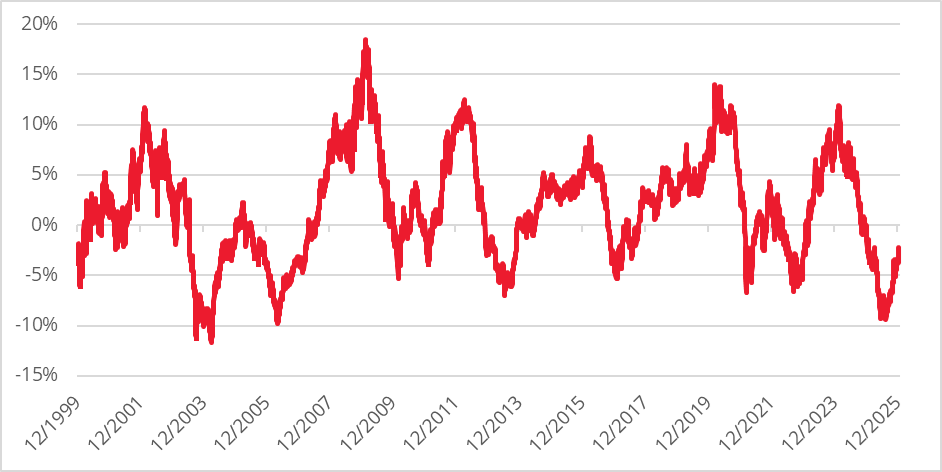

As 2025 ended, Quality stocks were in the grip of their worst period of relative underperformance in 20 years. The rolling one‑year performance of MSCI Quality versus MSCI World had sunk to -10% low in September, a sharp reversal from the highs seen in mid-2024, just before the Federal Reserve began to cut interest rates – see Chart 1.

It is tempting to see this as an opportunity to simply buy the dip and return to managers who put Quality front and centre, whatever the price. However, the Redwheel Global Equity Income team would argue that the world has changed: disruption is now too pervasive for ‘Quality for Quality’s sake’ to remain a workable approach.

Chart 1: MSCI Quality vs MSCI World – % relative rolling 1-year total return

Disruption is challenging ‘Quality at any price’

Traditional approaches to Quality lean heavily on what has gone right so far. Strong historic profitability, high returns on capital and long records of growth are treated as robust markers of future resilience. Yet the corporate landscape continues to shift under our feet. An EY study [1] highlighted that the average lifespan of an S&P 500 company has fallen from around 60–70 years in the mid‑twentieth century to just 15 years today, as competitive pressures, technology and capital markets shorten corporate lives.

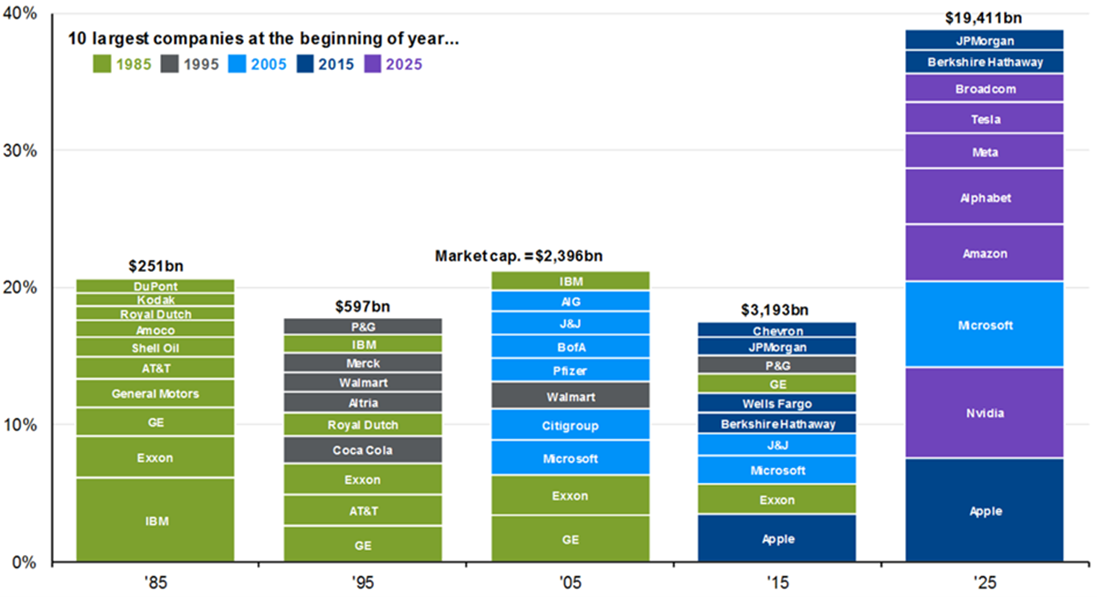

That shortening lifespan is not confined to old‑economy industries. The JP Morgan chart below showing the churn in the largest companies in the S&P 500 over successive decades underlines how quickly today’s champions can be displaced, even at the very top of the index.

Chart 2: Top 10 largest S&P 500 companies by decade

The recent software sell‑off is simply the latest expression of this trend. New AI tools and business models have raised legitimate questions about the durability of parts of the software‑as‑a‑service universe, triggering a broad de‑rating across companies previously regarded as near‑automatic winners. [2]

In this world, relying on historic quality characteristics to reassert themselves is increasingly hazardous. Business models that once looked almost immune to disruption – including those built on intellectual capital and recurring revenues – are now being challenged. The label “quality” tells you a lot about where a company has come from, but we argue that it shows much less about whether it can adapt, and at what price it still makes sense to own.

A more nuanced approach to Quality

Against that backdrop, the Global Equity Income team believes that two extra ingredients are essential: valuation and a repeatable way of judging whether disruption is temporary or permanent.

The strategy starts from a simple, objective rule. Every holding must yield at least 25% more than the MSCI World Index at purchase, and any stock whose prospective yield falls below the index must be sold within six months. That discipline ensures that the portfolio compounds a premium income stream relative to the market and prevents style shift towards overpriced growth stocks.

Quality businesses therefore only fall into the strategy’s investable universe when they are under pressure – when controversy has pushed the price down, the yield up and consensus towards the exit. At that point, the central question is not “is this a quality company?” but “is this a quality investment at this price, given what might change?” Years of deliberately exploiting such situations have created a practical library of repeating patterns that that team can use to distinguish between problems that are temporary or permanent.

The strategy’s recent ability to own Accenture [3] – historically too expensive on yield grounds – is a clear example of the opportunity created when a quality company’s share price falls 45% and its free cash flow moves above 5%.

Downside capture matters again

Each new idea is tested using structured checklists and scenario work to assess its ability to suffer change or drawdown. The focus is on a dual margin of safety: operational – can the business keep generating enough cash to support its dividend through a range of outcomes – and valuation – is the current price already discounting the worst, so that potential upside meaningfully outweighs the downside. If that asymmetry is missing, however tempting, they move on.

This approach has two implications for performance. It is likely to lag in euphoric periods when investors are happy to pay any price for perceived quality or growth leadership and when narrow themes dominate index returns. But when volatility returns – as it appears to be doing – and crowded trades unwind, the strategy’s focus on starting yield, durability and valuation has historically helped it protect capital and continue compounding income. Rather than treating volatility as something to be avoided, it becomes a source of opportunity as previously uninvestable names finally meet the strategy’s hurdle and downside capture matters again.

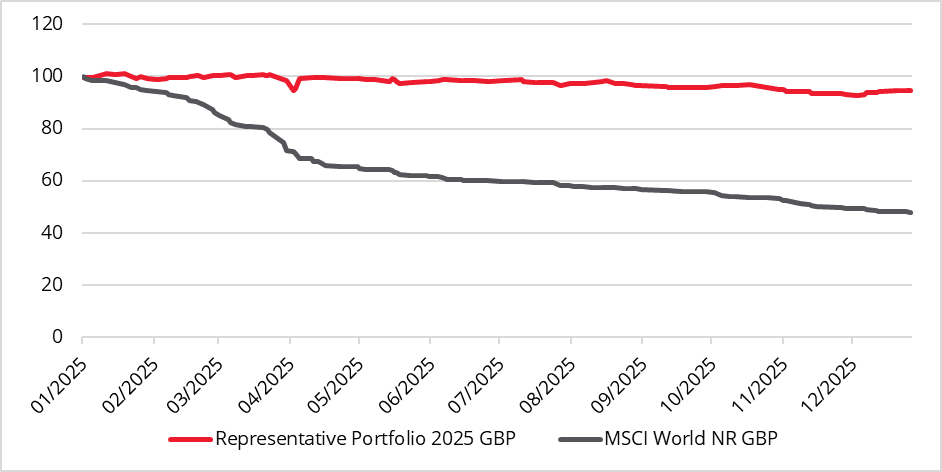

Chart 3: Representative portfolio vs MSCI World – performance over cumulative down days

Why this framework matters in the age of AI

The current AI revolution is a good example of why this framework matters for Quality investors. The first phase of enthusiasm has centred on the “picks and shovels” of the new wave – infrastructure, platforms and tools that promise to reshape how the economy works. As competition intensifies and the technology diffuses, the team believe AI is likely to move towards a more commoditised stage, where the real value lies not in owning the tools but in using them to deliver better customer service at lower costs, deepen competitive moats and drive strong cash flows.

As that transition unfolds, controversies will shift. Some current darlings may find their advantages eroded for good. Others, marked down in the recent sell‑off, may prove to be exactly the kind of durable, cash‑generative franchises that can harness new tools to reinforce their position. A global equity income strategy that insists on yield, durability and valuation – and is comfortable buying into controversy rather than crowding into comfort – is, we believe, well placed to distinguish between them.

Key Information

No investment strategy or risk management technique can guarantee returns or eliminate risks in any market environment. Past performance is not a guide to the future. The prices of investments and income from them may fall as well as rise and investors may not get back the full amount invested. Forecasts and estimates are based upon subjective assumptions about circumstances and events that may not yet have taken place and may never do so. The statements and opinions expressed in this article are those of the author as of the date of publication, and do not necessarily represent the view of Redwheel. This article does not constitute investment advice and the information shown is for illustrative purposes only.

References

[1] EY.com: ‘How businesses can stand the test of time’, June 2023

[2] Bloomberg, February 2025

[3] See ‘Good things come to those who wait’, Redwheel, November 2025