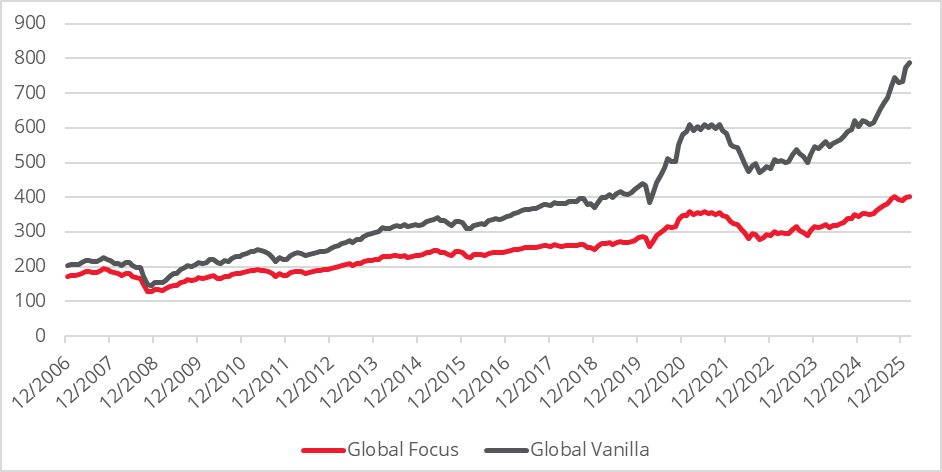

There are a few convertible bond indices that track the performance of the asset class but the most widely used are the ‘FTSE Global Vanilla Convertible Index’ (Vanilla) and the ‘FTSE Global Focus Convertible Index’ (Focus). However, while they both benchmark convertible bonds, their performance differential is so staggering that they almost represent two different asset classes. Think S&P versus NASDAQ or TOPIX versus Nikkei – and you are not even close. In fact, the Vanilla index has outperformed the Focus by a factor of more than two over the past 20 years.

Chart 1: FTSE Global Vanilla Convertible Index vs Global Focus – long-term performance

How do the indices differ?

There are a number of differences but by far the most relevant is the Focus index’s monthly rebalancing process that aims to remove the convertibles that are too high in price (very equity sensitive) and too low in price (very bond like). The Focus index therefore focuses on the balanced portion of the universe. The Vanilla index does not have this process of rebalancing and bonds are not removed from the index until conversion, maturity or bankruptcy.

How do the differences affect exposures?

The Vanilla index tends to exhibit a much higher equity sensitivity, given that bonds are not removed based on price appreciation. The correlation with equities therefore tends to be much higher and more volatile. The Focus index tends to be a lower volatility product which aims to have a higher ratio of upside participation to downside decline and tends to offer better diversification within broader asset allocation portfolios. It is essentially replicating a balanced portfolio of bonds and equities with the benefit of convexity, which simply means that investors tend to benefit more in a rising market than they lose in a declining market.

Which environments favour each index?

The Vanilla index tends to excel over longer cycles with continually rising, low-volatility equity markets and stable interest rates. In these conditions, its bonds are more likely to convert or mature after a rally than decline in price in a shorter cycle. The Focus index, however, tends to benefit in a more volatile market environment with shorter market cycles, as bonds are more likely to be reintroduced to indices after being removed due to price moves. Both indices, however, are likely to benefit from high primary market activity, sectoral biases towards growth and Small/Mid to Large cap outperformance over Mega Cap stocks

Which approach should investors choose?

The choice of index follows directly from the investor’s reason for allocating to convertible bonds. For investors looking at the asset class opportunistically based on valuation or primary market activity, either index could be suitable. For investors looking for an equity-like investment with a degree of capital preservation, who are not concerned with drawdowns or volatility and feel that upside in equity markets is more likely, then the Vanilla approach may be more suitable. For investors that feel that a more volatile environment is likely with upside being less momentum driven, the Focus approach would be more appropriate, in our view. Additionally, the Focus approach tends to be a better diversifier within multi-asset portfolios and fits better within overall asset allocation models. For investors that are considering allocating away from High yield, then the Focus approach could be considered as a good replacement. Generally, we feel that asset class’s key attributes of upside participation with a good degree of capital preservation is better represented in the Focus approach and efficiently represents a balanced portfolio.

A more efficient way to allocate to convertibles using both indices

Investing in convertible bonds is an active decision informed by a clear understanding the asset class, careful analysis of index performance and the investor’s view of the market environment. Choosing the right instrument to express a particular investment style can be challenging, not least because active managers are prone to style drift and significant deviations from index returns. Given that the decision to allocate to the asset class is already an active one, a passive implementation is a valid option.

In the Vanilla space, we know of only a handful of solutions available in the market which may work well. However, the Focus index has proved much harder to replicate given the constant rebalancing required and we know of even fewer solutions. We think that active allocators could add significant value by introducing convertibles into their strategic asset allocation, exploiting the structural efficiency of the asset class and then incrementally adding value by switching between the two approaches in line with their market view

Key Information

No investment strategy or risk management technique can guarantee returns or eliminate risks in any market environment. Past performance is not a guide to the future. The prices of investments and income from them may fall as well as rise and investors may not get back the full amount invested. Forecasts and estimates are based upon subjective assumptions about circumstances and events that may not yet have taken place and may never do so. The statements and opinions expressed in this article are those of the author as of the date of publication, and do not necessarily represent the view of Redwheel. This article does not constitute investment advice and the information shown is for illustrative purposes only.