We use strictly necessary cookies to enable our site to work and performance cookies to improve the visitor experience when visiting the site. We will only set performance cookies if you permit us to.

For more detailed information about the cookies we use, see the „Cookie Usage“ section of our Privacy Policy

Wandelanleihen bieten eine hybride Lösung für Anleger, die ein ausgewogenes Engagement am Finanzmarkt wünschen, welches die Vorteile von Aktien und Anleihen kombiniert. Seit mehr als einem Jahrzehnt verwendet unser Team proprietäre Modelle und Systeme, um die attraktivsten Chancen innerhalb dieser Anlageklasse zu identifizieren. Wir bieten eine Auswahl an aktiv verwalteten Lösungen, welche darauf ausgelegt sind, das attraktive, asymmetrische Renditeprofil von Wandelanleihen mit unterschiedlichen Risikotoleranzen zu nutzen.

Das Ecofin-Team verwaltet eine Reihe globaler thematischer Aktienstrategien mit dem Ziel, den Kunden hohe risikobereinigte Renditen zu bieten und gleichzeitig einige der größten ökologischen Herausforderungen unseres Planeten anzugehen, wie die Dekarbonisierung der Energieversorgung und der Infrastruktur.

Wir investieren in eine kleine Auswahl hochwertiger europäischer Unternehmen, bei denen wir durch die Lösung bestimmter unternehmensspezifischer Probleme potenziell bedeutende Möglichkeiten zur Schaffung von Mehrwert erkennen. Wir wirken als Katalysator für Veränderungen, indem wir konstruktiv mit den Unternehmen und mit anderen Aktionären zusammenarbeiten.

Ein sehr erfahrenes Team mit einer nachgewiesenen Erfolgsbilanz bei der Erzielung positiver Ergebnisse für Anleger. Die bewährte Anlagemethode, die Dividendenkraft der Titel voll auszuschöpfen, bietet das Potential, langfristig mehr Rendite bei unterdurchschnittlichen Volatilitätsraten einzufahren. Das Team ist sucht gezielt nach der seltenen Kombination aus hohen Renditen, nachhaltigen Dividenden und einer attraktiven Bewertung, welche nur dann auftritt, wenn es gewisse Kontroversen gibt. Indem wir alles daran setzen, diese Kontroveren im Kern zu verstehen, erhöhen wir für Sie aktiv die Wahrscheinlichkeit eines Investitionserfolges.

Japan ist die drittgrösste Volkswirtschaft der Welt. Die Unternehmenslandschaft des Landes befindet sich seit einigen Jahren im Umbruch. Durch unser Joint Venture mit dem in Tokio ansässigen Nissay Asset Management (NAM) investieren wir in eine kleine Anzahl ausgewählter japanischer Unternehmen, deren Bewertung aufgrund von Faktoren, welche wir für korrigierbar halten, nicht ihr volles Potenzial widerspiegelt. Wir agieren für diese Unternehmen als Partner im Change-Prozess, damit der Wandel, der zur Freisetzung des Potenzials notwendig ist, vollzogen werden kann.

Nachhaltigkeit im weitesten Sinne verändert das Anlageumfeld strukturell – sowohl von der Risiko- als auch von der Chancenbetrachtung her betrachtet. Das Redwheel Sustainable Growth Team ist bestrebt, strukturelle längerfristige Themen und Dynamiken in der Wirtschaft und der Gesellschaft zu identifizieren.

Unser Nachhaltigkeitsansatz bei der Anlagetätigkeit beruht auf drei Säulen: einer soliden Unternehmensführung und einem strengen Richtlinien Regelwerk für alle Redwheel-Fonds, einer zentralisierten Stewardship-Expertise für unsere Anlageteams, von denen jedes sein eigenes individuelles Engagement für die Unternehmen, in die es investiert, durchführt, und Greenwheel, unserem hauseigenen Team von Experten für Nachhaltigkeitsresearch.

Die Abteilung ‚Stewardship and Regulatory Change‘ von Redwheel ist für die operative Unterstützung des Stewardship bei Redwheel zuständig.

Das Team für Nachhaltigkeitsstrategie, Governance und Richtlinien berät und unterstützt Redwheel und seine Anlageteams bei der Integration von Nachhaltigkeitsaspekten in die Anlageprozesse und trägt dazu bei, dass sich Redwheel‘s Ansatz für verantwortungsbewusste Anlagen im Einklang mit den Kundenbedürfnissen und regulatorischen Anforderungen weiterentwickelt.

Greenwheel ist der Partner für die Nachhaltigkeitsanalysen der Redwheel-Fonds ‘Sustainable, Transition und Enhanced Integration’. Greenwheel bietet Redwheel-Fondsmanagern in jeder Phase des Lebenszyklus nachhaltiger Produkte maßgeschneidertes Nachhaltigkeits-Research und Beratung auf thematischer und sektoraler Ebene, von der Fondsgestaltung bis hin zu Investment-Research und Engagement-Unterstützung, abhängig von den Bedürfnissen und Anforderungen des jeweiligen Teams. Das von den Fondsmanagern in Auftrag gegebene Modell gewährleistet, dass das Research auf das Anlageprodukt und das Kundenergebnis zugeschnitten ist

As traditional global growth engines falter and market multiples remain compressed across many developed economies, a wave of reforms – from financial system liberalisation to robust governance improvements – is transforming developing economies. Markets that once lagged global indices are now demonstrating credible steps towards transparency and competitiveness – unlocking compelling value for investors.

Against this backdrop, South Korea and South Africa stand out for their ongoing reform momentum, deepening capital markets and rerating potential.

The Redwheel Emerging Markets Equity strategy maintains a marginal overweight in Korea at 10.9% [1], mirroring the MSCI Emerging Markets index, but concentrated in high-conviction areas, including semiconductors, banks, industrials, and ecommerce. Performance year to date supports this thesis, with the MSCI Korea Index surging 44.8% in USD terms, led by capital goods and industrials (+82.8%), financials (+53%), and Information Technology (+46%), and supported by a 5.3% appreciation of the South Korean won [2].

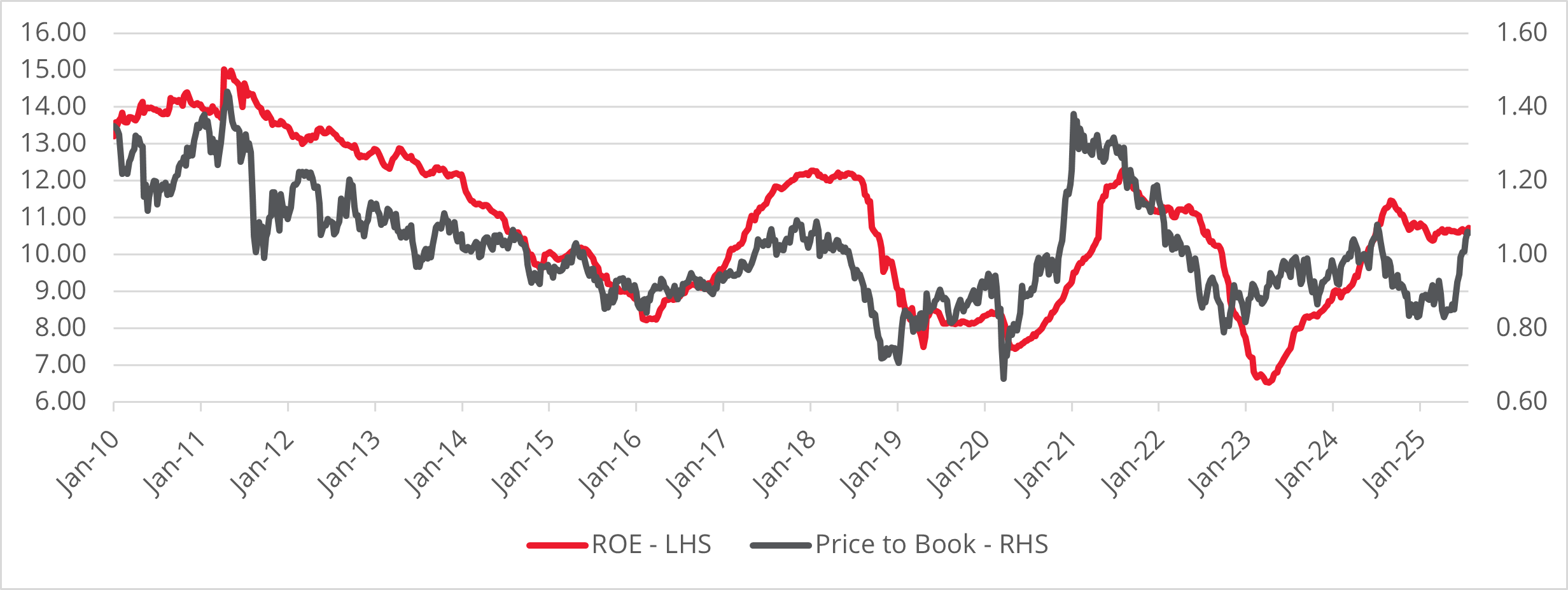

However, despite the rally year-to-date, valuations remain below historical averages with the MSCI Korea index trading at 1x price to book (P/B) for 11% return on equity (ROE) [3]. The team believes that the new prime minister’s target of driving the KOSPI index from 3072 (as of 30 June) to 5000 [4] is achievable in light of an ambitious reform program to improve equity market returns.

Chart 1: MSCI Korea index – Price to book vs return on equity

Corporate reform: Unlocking shareholder value

Korea has historically lagged in corporate governance standards compared to developed market peers. The “Corporate Value-up” program, now in its second year, aims to improve transparency, capital efficiency, and minority shareholder rights in a bid to encourage greater domestic retail participation and foreign capital flows, ultimately reducing the “Korea discount.”

A notable policy shift involves the treatment of share buybacks. Historically, companies repurchased shares and kept them as treasury stock, often for non-commercial purposes beneficial to controlling shareholders. Recent regulatory changes aim to ensure surplus capital is returned to shareholders more efficiently – either through outright cancellation of treasury shares or redistribution via dividends.

Share buybacks and cancellations typically drive earnings multiple expansion as outstanding share count is reduced relative to earnings. It is estimated that treasury shares account for a significant percentage (4%) of corporate share counts on average [5]. Share cancellations would therefore have a material impact on valuations across the country index while preventing management from using treasury shares for non-economic purposes.

Another important policy reform concerns dividend tax reduction. The draft dividend tax reduction law improves the attractiveness of dividend income and aims to cultivate a more stable and engaged investor base in South Korea’s equity market.

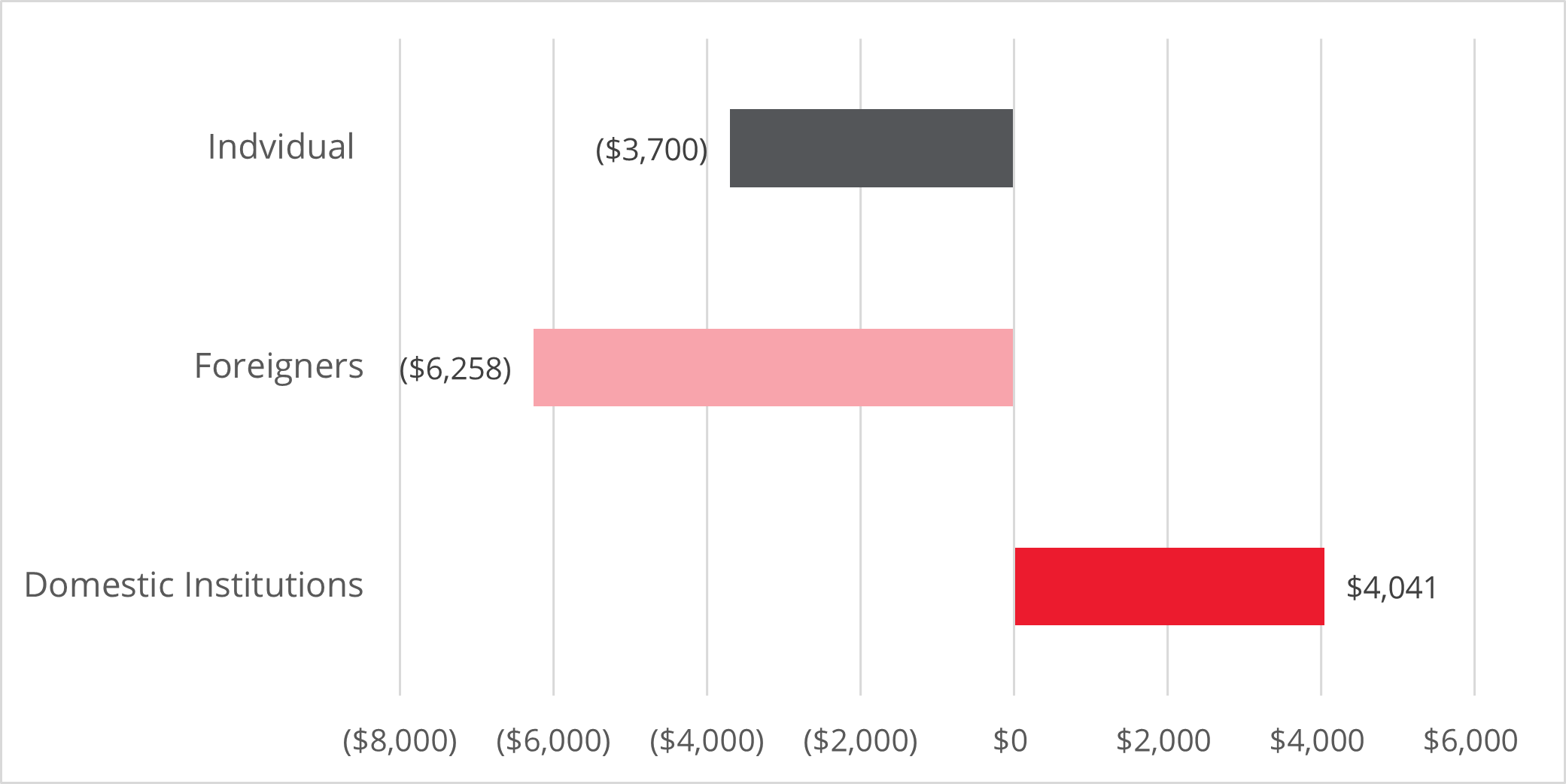

Recent flows highlight a favourable domestic reception to the reforms. The rally year-to-date was driven largely by domestic institutional flows even though foreign investors were net sellers.

Chart 2: Korea investor flows, 2025 YTD (USD millions)

Samsung Electronics: Leading reform and setting the benchmark

Samsung Electronics stands at the forefront of South Korea’s corporate reform. The first to introduce buybacks in Korea, Samsung has bought back shares worth KRW20 trillion since 2015 and increased dividends on a steady basis since then [6]. As the new dividend tax regime takes effect, this could increase further.

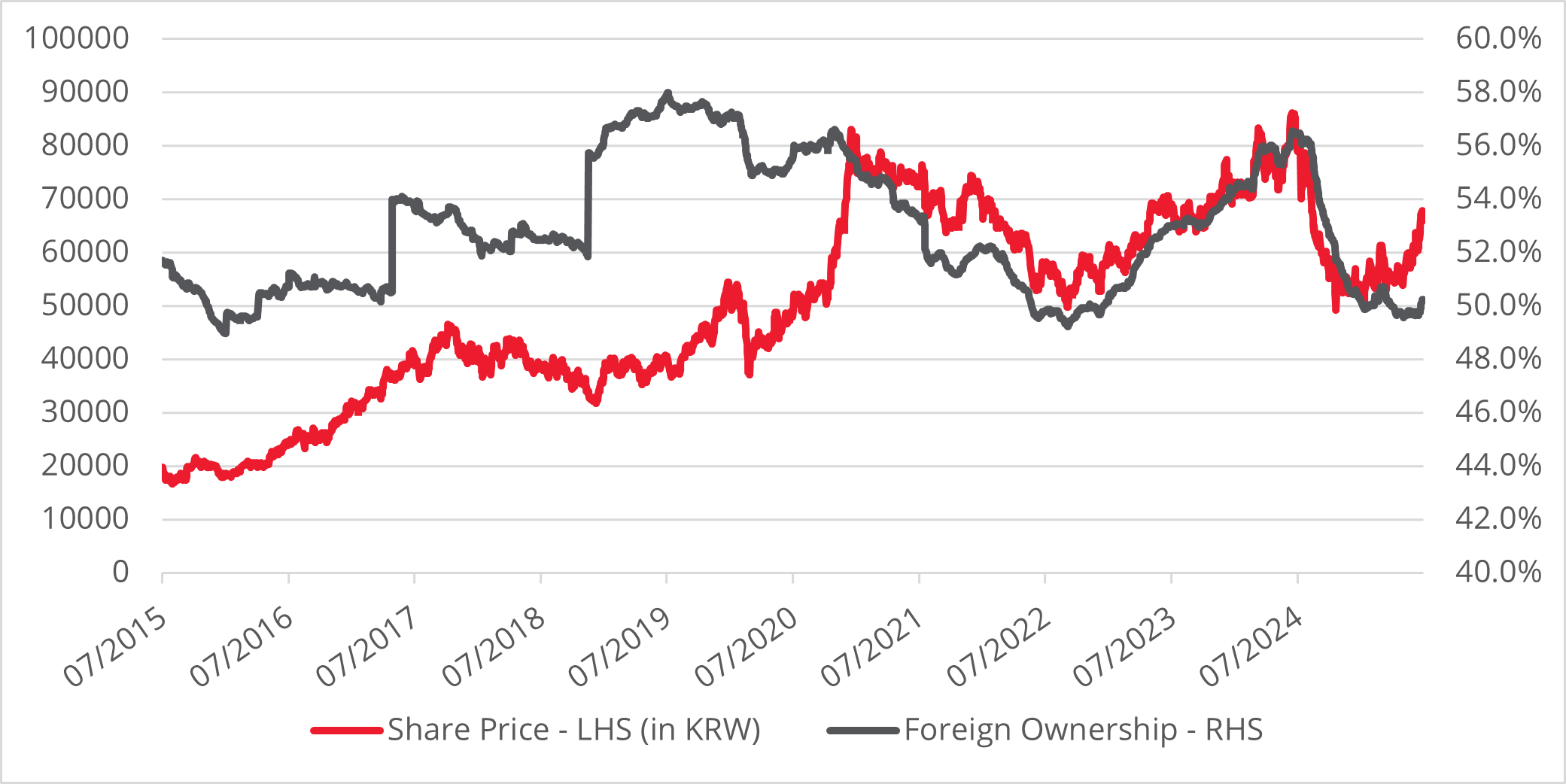

Despite a robust net cash position [7] and strong increases in the price of memory [8], the stock trades on a low multiple of 11x 2025E P/E (a 20% discount to global semiconductors) even after its 23% rally to mid-year.] Both domestic and foreign investors remain underweight [8] but, as the largest stock in the index (22.3% [10]), a change in sentiment will be essential to drive a country rerating.

Chart 3: Samsung Electronics – price vs foreign ownership

Banks: Deep value and dividend upside

Korean banks currently offer some of the most attractive value opportunities globally. Despite robust earnings and improving ROE, the sector trades at just 0.6x P/B: a steep discount versus international peers [11]. Moreover, Korea remains one of the last major markets where banks trade below book value, while similar cycles of revaluation in Europe and Japan have already seen bank multiples converge towards or above book [10]. If Korean banks rerate towards book value, the team believes that stocks could see up to 50% additional upside.

The dividend outlook for the sector remains exceptional. Leading banks are aggressively returning capital to shareholders, with expected average dividend yields exceeding 7% and payout ratios as low as 26% – 30% [10].

Finally, stock cancellations could provide another tailwind for both flows and valuations: recent announcements from the top four banks indicate that cancellations could amount to USD2.5bn in 2025 [12].

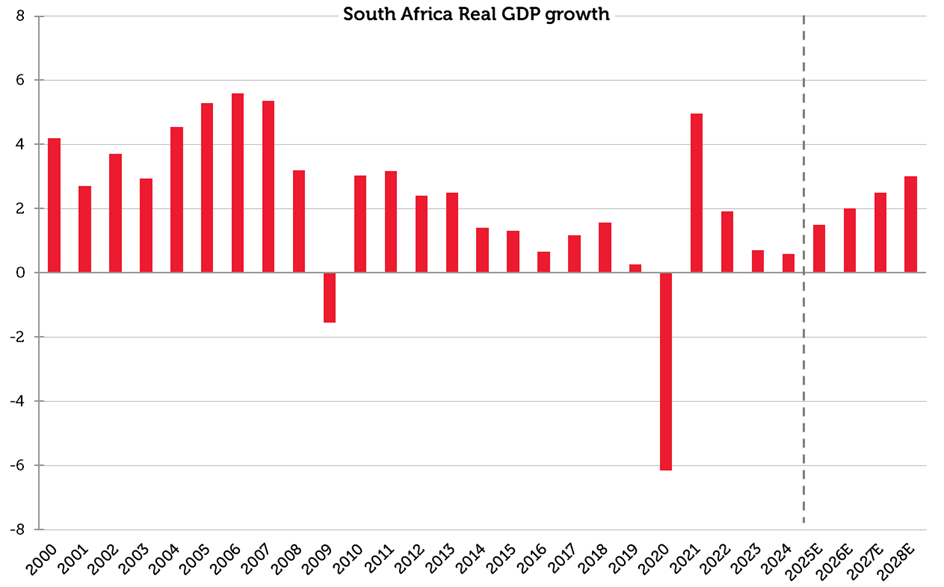

The team continues to reflect a strong conviction in South Africa, maintaining an overweight portfolio allocation of 10.5%, substantially higher than the MSCI Emerging Markets index weighting (2.9%).[13] After a decade of sluggish growth, there are clear signs of GDP acceleration on the horizon – see chart 4, supported by falling inflation and interest rates. South African CPI has fallen from 8% post pandemic to 2.8% at the end of May [14].

Chart 4: South Africa – Real GDP growth (%)

The MSCI South Africa valuation has de-rated by around 45% [15] since its last upcycle in 2015, and valuations now look very attractive, despite climbing over 30% in the first half of the year [16], propelled by USD weakness and robust metals prices. The MSCI South Africa index is trading at a 20% discount relative to the MSCI EM index on a historical long-term average basis [15].

A key factor in this improving outlook is the emergence of a more business-friendly government following the May 2024 elections. The Government of National Unity has publicly pledged to eradicate corruption and inefficiency. Addressing neglected infrastructure is high on the political agenda, setting the stage for a structural rebound in economic performance and investor confidence. It also aims to restore the operational reliability of Eskom, the national electric utility, which should drive a continued recovery in electricity production, supporting industry and mining.

Platinum group metals and gold: price tailwinds

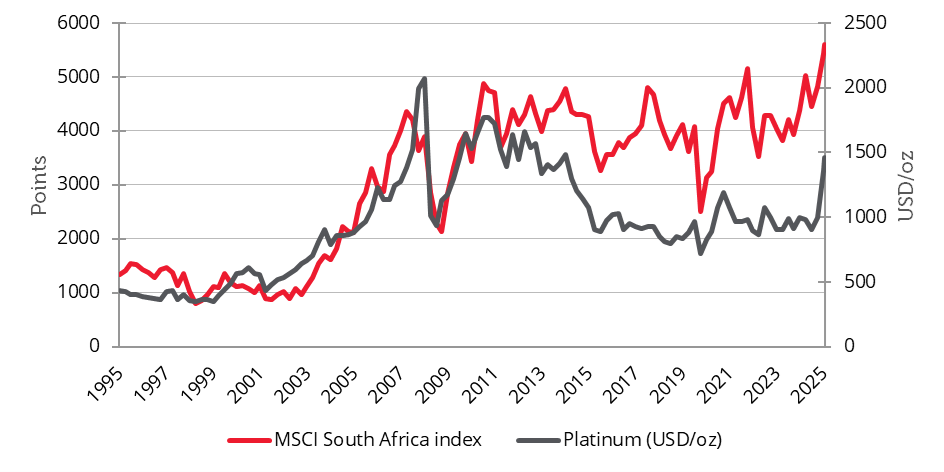

South Africa also benefits from a positive pricing environment for precious metals. The country is the world’s largest producer of platinum group metals (PGMs), commanding a 45% share of global output.[17] Higher prices and tightening supply—driven by underinvestment, stricter Chinese auto-catalyst regulations, and growing platinum jewellery use—are reinforcing the prospects of leading local producers such as Impala Platinum and Valterra Platinum. The chart below highlights the strong influence of PGM prices on South African valuations.

Chart 5: MSCI South Africa index stock vs Platinum price per ounce

Gold also shines on the back of a weakening US dollar and global trade tensions, further boosting earnings for portfolio holdings like Gold Fields and AngloGold Ashanti. [18] These firms benefit not just from current price trends but also from successful mine development projects across Africa.

Telecoms: Driving financial inclusion through mobile money

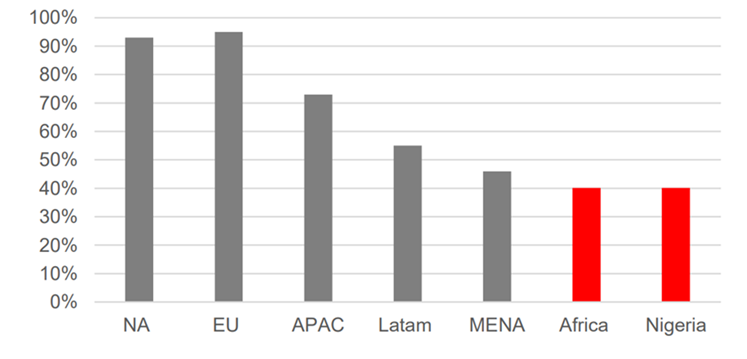

The team’s holding in MTN, the largest telecom company in Africa, climbed 69% in USD terms to mid-year. Banking penetration in Africa remains very low – see Chart 6, and the team is seeing a strong trend of industry leapfrogging, as telecom operators drive financial inclusion through mobile money transfers that are substituting cash payments. MTN’s fintech division accounts for a rising share of group revenues [19] and the team expects the company to deliver strong growth from its high margin, highly scalable mobile money platform.

Chart 6: Traditional banking penetration

Financial sector: Private sector credit growth

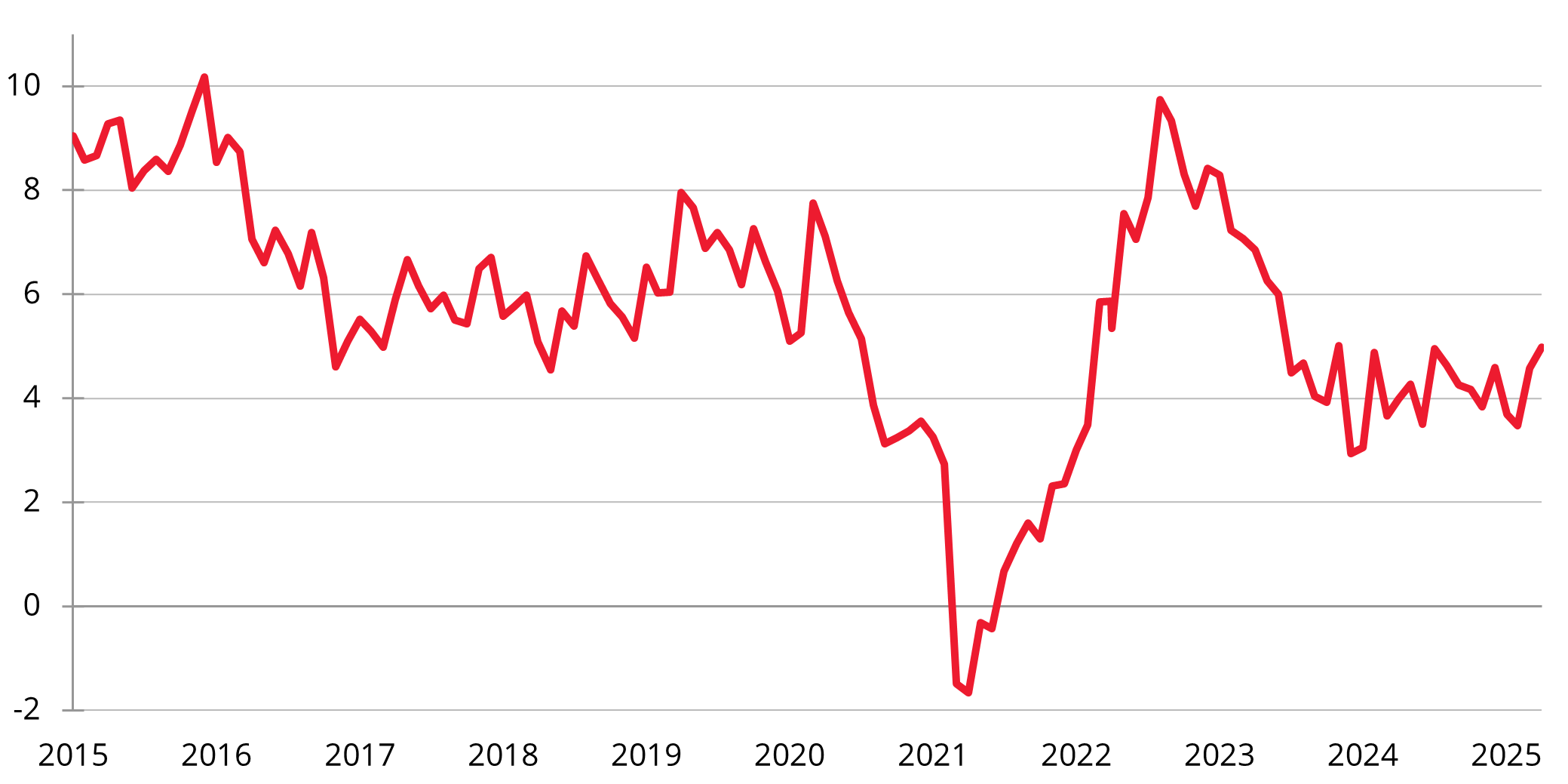

Against an improving economic backdrop, the team expects domestic banks to benefit from stronger loan growth (see Chart 7) over the coming year, translating into double-digit earnings growth as interest rates decline and corporate capex recovers. The team’s two South African banking holdings are Capitec and Standard Bank. Capitec has proven to be a disruptive force in the financial sector by delivering highly competitive products to under-served market segments. Standard Bank, the largest bank in Africa, stands to gain from increased corporate investment and the wider upturn in the commodity cycle.

Chart 7: South Africa credit extension to private sector (YoY %)

Reform as a rerating catalyst

Both South Korea and South Africa exemplify the investment case for frontier and next generation emerging markets at a time when reform and restructuring serve as powerful rerating catalysts. In South Korea, the convergence of regulatory enhancements, buyback transparency, and deep-value banking stocks points to meaningful rerating potential. In South Africa, the new coalition government signals an encouraging break from the past, with a pragmatic focus on addressing long-standing impediments to growth and investor confidence.

With disciplined, index-agnostic portfolios and a focus on growth at a reasonable price, the team believes that it is well positioned to capture potential upside from both earnings recovery and currency appreciation.

Key Information

No investment strategy or risk management technique can guarantee returns or eliminate risks in any market environment. Past performance is not a guide to the future. The prices of investments and income from them may fall as well as rise and investors may not get back the full amount invested. Forecasts and estimates are based upon subjective assumptions about circumstances and events that may not yet have taken place and may never do so. The statements and opinions expressed in this article are those of the author as of the date of publication, and do not necessarily represent the view of Redwheel. This article does not constitute investment advice and the information shown is for illustrative purposes only.

[1] Redwheel, 28 July 2025

[2] Bloomberg, 31 July 2025

[3] Bloomberg, 24 July 2025

[5] UBS report, 9 July 2025

[6] Bloomberg, 23 July 2025

[8] DRAMExchange.com, 22 July 2025

[9] Bloomberg, 24 July 2025

[10] Bloomberg, 30 July 2025

[11] Bloomberg consensus estimates, 24 July 2025

[12] Company announcements: KB Financial (24.07.25); Shinhan Financial (25.07.25); Hana Financial (25.07.25); Woori Financial (25.07.25)

[13] Bloomberg, 30 June 2025

[14] Bloomberg, 31 May 2025

[15] Bloomberg, 23 July 2025

[16] Bloomberg, 31 July 2025

[17] Bloomberg, 23 July 2025

[18] Bloomberg, 23 July 2025

[19] Company report for quarter ending 31 March 2025

Discover how our Ecofin investment team argues that disruption in the Strait of Hormuz could be an energy shock with echoes of Fukushima, reshaping global power markets and energy security priorities.

There is an old Warren Buffett quote that is often used: “Price is what you pay, value is what you get”. Most investors nod along and then go back to buying whatever US large-cap growth stock everyone else is buying. Large mispricings are more likely to be found in areas where few are looking, however, and this should prompt the bargain hunter to start peering into places far from New York and London...

Watch the latest video from Portfolio Manager, Davide Basile, to learn more about Redwheel's Enhanced Index Focus Convertibles Strategy.

Redwheel ® and Ecofin ® are registered trademarks of RWC Partners Limited (“RWC”). The term “Redwheel” may include any one or more Redwheel branded regulated entities including RWC Asset Management LLP, which is authorised and regulated by the UK Financial Conduct Authority and the US Securities and Exchange Commission (“SEC”); RWC Asset Advisors (US) LLC, which is registered with the SEC; RWC Singapore (Pte) Limited, which is licensed as a Licensed Fund Management Company by the Monetary Authority of Singapore; Redwheel Australia Pty Ltd is an Australian Financial Services Licensee with the Australian Securities and Investment Commission; and Redwheel Europe Fondsmæglerselskab A/S which is regulated by the Danish Financial Supervisory Authority.

Redwheel may act as investment manager or adviser, or otherwise provide services, to more than one product pursuing a similar investment strategy or focus to the product detailed in this document. Redwheel and RWC (together “Redwheel Group”) seeks to minimise any conflicts of interest, and endeavours to act at all times in accordance with its legal and regulatory obligations as well as its own policies and codes of conduct.

This document is directed only at professional, institutional, wholesale or qualified investors. The services provided by Redwheel are available only to such persons. It is not intended for distribution to and should not be relied on by any person who would qualify as a retail or individual investor in any jurisdiction or for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to local law or regulation.

This document has been prepared for general information purposes only and has not been delivered for registration in any jurisdiction nor has its content been reviewed or approved by any regulatory authority in any jurisdiction.

The information contained herein does not constitute: (i) a binding legal agreement; (ii) legal, regulatory, tax, accounting or other advice; (iii) an offer, recommendation or solicitation to buy or sell shares in any fund, security, commodity, financial instrument or derivative linked to, or otherwise included in a portfolio managed or advised by Redwheel; or (iv) an offer to enter into any other transaction whatsoever (each a “Transaction”). Redwheel Group bears no responsibility for your investment research and/or investment decisions and you should consult your own lawyer, accountant, tax adviser or other professional adviser before entering into any Transaction. No representations and/or warranties are made that the information contained herein is either up to date and/or accurate and is not intended to be used or relied upon by any counterparty, investor or any other third party.

Redwheel Group uses information from third party vendors, such as statistical and other data, that it believes to be reliable. However, the accuracy of this data, which may be used to calculate results or otherwise compile data that finds its way over time into Redwheel Group research data stored on its systems, is not guaranteed. If such information is not accurate, some of the conclusions reached or statements made may be adversely affected. Any opinion expressed herein, which may be subjective in nature, may not be shared by all directors, officers, employees, or representatives of Group and may be subject to change without notice. Redwheel Group is not liable for any decisions made or actions or inactions taken by you or others based on the contents of this document and neither Redwheel Group nor any of its directors, officers, employees, or representatives (including affiliates) accepts any liability whatsoever for any errors and/or omissions or for any direct, indirect, special, incidental, or consequential loss, damages, or expenses of any kind howsoever arising from the use of, or reliance on, any information contained herein.

Information contained in this document should not be viewed as indicative of future results. Past performance of any Transaction is not indicative of future results. The value of investments can go down as well as up. Certain assumptions and forward looking statements may have been made either for modelling purposes, to simplify the presentation and/or calculation of any projections or estimates contained herein and Redwheel Group does not represent that that any such assumptions or statements will reflect actual future events or that all assumptions have been considered or stated. There can be no assurance that estimated returns or projections will be realised or that actual returns or performance results will not materially differ from those estimated herein. Some of the information contained in this document may be aggregated data of Transactions executed by Redwheel that has been compiled so as not to identify the underlying Transactions of any particular customer.

No representations or warranties of any kind are intended or should be inferred with respect to the economic return from, or the tax consequences of, an investment in a Redwheel-managed fund.

This document expresses no views as to the suitability or appropriateness of the fund or any other investments described herein to the individual circumstances of any recipient.

The information transmitted is intended only for the person or entity to which it has been given and may contain confidential and/or privileged material. In accepting receipt of the information transmitted you agree that you and/or your affiliates, partners, directors, officers and employees, as applicable, will keep all information strictly confidential. Any review, retransmission, dissemination or other use of, or taking of any action in reliance upon, this information is prohibited. Any distribution or reproduction of this document is not authorised and is prohibited without the express written consent of Redwheel Group.

Funds managed by Redwheel are not, and will not be, registered under the Securities Act of 1933 (the “Securities Act”) and are not available for purchase by US persons (as defined in Regulation S under the Securities Act) except to persons who are “qualified purchasers” (as defined in the Investment Company Act of 1940) and “accredited investors” (as defined in Rule 501(a) under the Securities Act).

This document does not constitute an offer to sell, purchase, subscribe for or otherwise invest in units or shares of any fund managed by Redwheel. Any offering is made only pursuant to the relevant offering document and the relevant subscription application. Prospective investors should review the offering memorandum in its entirety, including the risk factors in the offering memorandum, before making a decision to invest.

AIFMD and Distribution in the European Economic Area (“EEA”)

The Alternative Fund Managers Directive (Directive 2011/61/EU) (“AIFMD”) is a regulatory regime which came into full effect in the EEA on 22 July 2014. RWC Asset Management LLP is an Alternative Investment Fund Manager (an “AIFM”) to certain funds managed by it (each an “AIF”). The AIFM is required to make available to investors certain prescribed information prior to their investment in an AIF. The majority of the prescribed information is contained in the latest Offering Document of the AIF. The remainder of the prescribed information is contained in the relevant AIF’s annual report and accounts. All of the information is provided in accordance with the AIFMD.

In relation to each member state of the EEA (each a “Member State”), this document may only be distributed and shares in a Redwheel fund (“Shares”) may only be offered and placed to the extent that (a) the relevant Redwheel fund is permitted to be marketed to professional investors in accordance with the AIFMD (as implemented into the local law/regulation of the relevant Member State); or (b) this document may otherwise be lawfully distributed and the Shares may lawfully be offered or placed in that Member State (including at the initiative of the investor).

Information Required for Offering in Switzerland of Foreign Collective Investment Schemes to Qualified Investors within the meaning of Article 10 CISA.

This is an advertising document.

The representative and paying agent of the Redwheel-managed funds in Switzerland (the “Representative in Switzerland”) FIRST INDEPENDENT FUND SERVICES LTD, Feldeggstrasse 12, CH-8008 Zurich. Swiss Paying Agent: Helvetische Bank AG, Seefeldstrasse 215, CH-8008 Zurich. In respect of the units of the Redwheel-managed funds offered in Switzerland, the place of performance is at the registered office of the Swiss Representative. The place of jurisdiction is at the registered office of the Swiss Representative or at the registered office or place of residence of the investor.

Redwheel ® and Ecofin ® are registered trademarks of RWC Partners Limited. The term “Redwheel” may include any one or more Redwheel regulated entities including RWC Asset Management LLP, which is authorised and regulated by the Financial Conduct Authority in the United Kingdom (“RWC”). RWC is incorporated in England and Wales with its registered office at Verde 4th Floor, 10 Bressenden Place, London, SW1E 5DH, United Kingdom and its registered number is OC332015.

No investment strategy or risk management technique can guarantee returns or eliminate risks in any market environment.The term “RWC” may include any one or more RWC branded entities including RWC Partners Limited and RWC Asset Management LLP, each of which is authorised and regulated by the UK Financial Conduct Authority and, in the case of RWC Asset Management LLP, the US Securities and Exchange Commission; RWC Asset Advisors (US) LLC, which is registered with the US Securities and Exchange Commission; and RWC Singapore (Pte) Limited, which is licensed as a Licensed Fund Management Company by the Monetary Authority of Singapore.RWC may act as investment manager or adviser, or otherwise provide services, to more than one product pursuing a similar investment strategy or focus to the product detailed in this audio. RWC seeks to minimise any conflicts of interest, and endeavours to act at all times in accordance with its legal and regulatory obligations as well as its own policies and codes of conduct.This audio is directed only at professional, institutional, wholesale or qualified investors. The services provided by RWC are available only to such persons. It is not intended for distribution to and should not be relied on by any person who would qualify as a retail or individual investor in any jurisdiction or for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to local law or regulation.This audio has been prepared for general information purposes only and has not been delivered for registration in any jurisdiction nor has its content been reviewed or approved by any regulatory authority in any jurisdiction. The information contained herein does not constitute: (i) a binding legal agreement; (ii) legal, regulatory, tax, accounting or other advice; (iii) an offer, recommendation or solicitation to buy or sell shares in any fund, security, commodity, financial instrument or derivative linked to, or otherwise included in a portfolio managed or advised by RWC; or(iv) an offer to enter into any other transaction whatsoever (each a “Transaction”). No representations and/or warranties are made that the information contained herein is either up to date and/or accurate and is not intended to be used or relied upon by any counterparty, investor or any other third party.RWC uses information from third party vendors, such as statistical and other data, that it believes to be reliable. However, the accuracy of this data, which may be used to calculate results or otherwise compile data that finds its way over time into RWC research data stored on its systems, is not guaranteed. If such information is not accurate, some of the conclusions reached or statements made may be adversely affected. RWC bears no responsibility for your investment research and/or investment decisions and you should consult your own lawyer, accountant, tax adviser or other professional adviser before entering into any Transaction. Any opinion expressed herein, which may be subjective in nature, may not be shared by all directors, officers, employees, or representatives of RWC and may be subject to change without notice. RWC is not liable for any decisions made or actions or in actions taken by you or others based on the contents of this audio and neither RWC nor any of its directors, officers, employees, or representatives (including affiliates) accepts any liability whatsoever for any errors and/or omissions or for any direct, indirect, special, incidental, or consequential loss, damages, or expenses of any kind howsoever arising from the use of, or reliance on, any information contained herein.Information contained in this audio should not be viewed as indicative of future results. Past performance of any Transaction is not indicative of future results. The value of investments can go down as well as up. Certain assumptions and forward looking statements may have been made either for modelling purposes, to simplify the audio and/or calculation of any projections or estimates contained herein and RWC does not represent that that any such assumptions or statements will reflect actual future events or that all assumptions have been considered or stated. Forward-looking statements are inherently uncertain, and changing factors such as those affecting the markets generally, or those affecting particular industries or issuers, may cause results to differ from those discussed. Accordingly, there can be no assurance that estimated returns or projections will be realised or that actual returns or performance results will not materially differ from those estimated herein. Some of the information contained in this audio may be aggregated data of Transactions executed by RWC that has been compiled so as not to identify the underlying Transactions of any particular customer.The information transmitted is intended only for the person or entity to which it has been given and may contain confidential and/or privileged material. In accepting receipt of the information transmitted you agree that you and/or your affiliates, partners, directors, officers and employees, as applicable, will keep all information strictly confidential. Any review, retransmission, dissemination or other use of, or taking of any action in reliance upon, this information is prohibited. The information contained herein is confidential and is intended for the exclusive use of the intended recipient(s) to which this audio has been provided. Any distribution or reproduction of this audio is not authorised and is prohibited without the express written consent of RWC or any of its affiliates.Changes in rates of exchange may cause the value of such investments to fluctuate. An investor may not be able to get back the amount invested and the loss on realisation may be very high and could result in a substantial or complete loss of the investment. In addition, an investor who realises their investment in a RWC-managed fund after a short period may not realise the amount originally invested as a result of charges made on the issue and/or redemption of such investment. The value of such interests for the purposes of purchases may differ from their value for the purpose of redemptions. No representations or warranties of any kind are intended or should be inferred with respect to the economic return from, or the tax consequences of, an investment in a RWC-managed fund. Current tax levels and reliefs may change. Depending on individual circumstances, this may affect investment returns. Nothing in this document constitutes advice on the merits of buying or selling a particular investment. This audio expresses no views as to the suitability or appropriateness of the fund or any other investments described herein to the individual circumstances of any recipient.AIFMD and Distribution in the European Economic Area (“EEA”)The Alternative Fund Managers Directive (Directive 2011/61/EU)(“AIFMD”) is a regulatory regime which came into full effect in the EEA on 22 July 2014. RWC Asset Management LLP is an Alternative Investment Fund Manager (an “AIFM”) to certain funds managed by it (each an “AIF”). The AIFM is required to make available to investors certain prescribed information prior to their investment in an AIF. The majority of the prescribed information is contained in the latest Offering Document of the AIF. The remainder of the prescribed information is contained in the relevant AIF’s annual report and accounts. All of the information is provided in accordance with the AIFMD.In relation to each member state of the EEA (each a “Member State”),this document may only be distributed and shares in a RWC fund(“Shares”) may only be offered and placed to the extent that (a) the relevant RWC fund is permitted to be marketed to professional investors in accordance with the AIFMD (as implemented into the local law/regulation of the relevant Member State); or (b) this audio may otherwise be lawfully distributed and the Shares may lawfully offered or placed in that Member State (including at the initiative of the investor).Information Required for Distribution of Foreign Collective Investment Schemes to Qualified Investors in SwitzerlandThe representative and paying agent of the RWC-managed funds in Switzerland (the “Representative in Switzerland”) FIRST INDEPENDENT FUND SERVICES LTD, Klausstrasse 33, CH-8008 Zurich. Swiss Paying Agent: Helvetische Bank AG, Seefeldstrasse 215, CH-8008 Zurich. In respect of the units of the RWC-managed funds distributed in Switzerland, the place of performance and jurisdiction is at the registered office of the Representative in Switzerland.