We use strictly necessary cookies to enable our site to work and performance cookies to improve the visitor experience when visiting the site. We will only set performance cookies if you permit us to.

For more detailed information about the cookies we use, see the “Cookie Usage” section of our Privacy Policy

Convertible bonds provide a hybrid solution for investors looking for a balanced exposure to financial markets that combines the attractive elements of both equities and bonds. For more than a decade, our team has been deploying its proprietary models and systems to help identify the most attractive opportunities within the asset class. We provide a range of actively managed solutions, designed to exploit the attractive asymmetric return profile of convertible bonds with varying degrees of risk tolerance.

Emerging and frontier markets represent the fastest growing economies in the world. We believe the continued growth of these markets presents compelling opportunities across a range of industries. Our index agnostic, opportunistic approach has been honed for more than two decades, and the depth of experience garnered within our team allows us to participate in attractive growth opportunities that are off the beaten track for most investors.

We invest in a small number of high-quality European companies, where we identify potentially significant opportunities to create additional value by addressing certain company-specific issues. We then act as a catalyst for change by constructively working together with the companies and other shareholders.

A highly experienced team with an established track record of delivering positive outcomes for investors. Harnessing the full power of dividends is a tried and tested method of investing, with the potential to deliver value added long-term returns and lower-than-average volatility. The team looks for the rare combination of a premium yield, sustainable dividend and attractive valuation, which only occurs when controversy appears. By working hard to understand the nature of a controversy, we aim to lean the probability of investment success in your favour.

Japan is the world’s third largest economy and its corporate landscape is undergoing dramatic change. Through our joint venture with Tokyo-based Nissay Asset Management (NAM), we invest in a small number of select Japanese companies that are not valued to their full potential due to factors we see as rectifiable. We then engage in order to act as an agent for the change required to unlock value.

Sustainability, in its broadest context, is structurally changing the investment landscape from both a risk and opportunities perspective. The Redwheel Sustainable Growth team seeks to identify structural longer-term themes and dynamics in the economy and society. The team invests capital to take advantage of the potential return opportunities these themes and dynamics offer, and to facilitate and further advance the positive impact of investee companies on critical sustainability challenges and development goals.

We are long-term value investors who believe that short-term factors prompt many market participants to overreact to news which may have little or no impact on the true value of a company. This causes share prices to diverge from the intrinsic value of the underlying business and provides an opportunity for long-term investors to purchase shares at an attractive discount. This builds in a margin of safety but also provides meaningful long-term total return potential through both dividend income and capital appreciation.

Redwheel is committed to facilitating and delivering responsible investment in practice. In line with their investment freedoms, each investment team is responsible for the integration of sustainability considerations within their respective investment processes, consistent with firm-level policies.

Redwheel’s stewardship function focuses primarily on overseeing and supporting the stewardship activities of our investment teams, co-ordinating our involvement in external stewardship initiatives, and leading in the development of the stewardship that Redwheel does as a corporate entity.

What is Sustainability Strategy, Governance & Policy? Sustainability Strategy, Governance and Policy focuses in three areas.

Greenwheel is the sustainability insights partner to Redwheel’s Sustainable, Transition and Enhanced Integration funds. Greenwheel provides tailored thematic and sector level sustainability research and advice to fund managers, commissioned by fund managers.

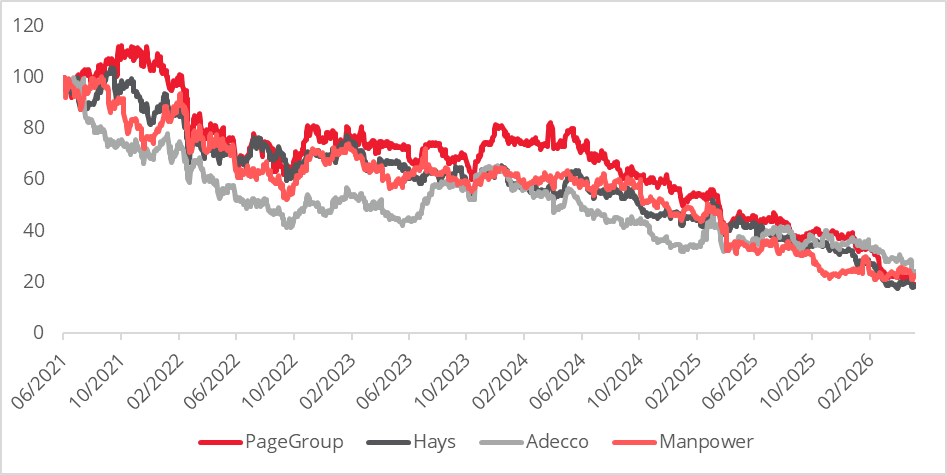

New, disruptive technologies tend to provoke the same investor response: a rush to simple narratives and indiscriminate selling across anything perceived to be in the firing line. We saw this in software earlier this year , and more recently in staffing and adjacent sectors, where fears of AI-driven disruption have driven share prices well beyond the fundamentals.

That logic has now spread into contract catering, where concerns over AI’s impact on office-based employment have cast a shadow over demand. In our view, this is a classic controversy – rooted in first-order thinking rather than fundamental reality – and one that has created an opportunity to invest in Compass Group , a high-quality business at an attractive valuation.

Chart 1 – Staffing company performance since 2021

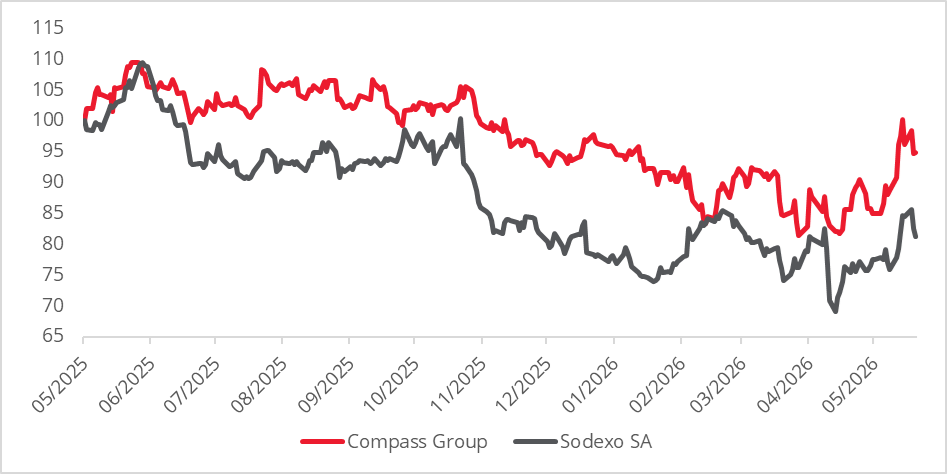

Compass Group was added to the Redwheel Global Equity Income strategy in Q1 2026, having fallen by around 30% over the previous 12 months and mostly since October 2025. The controversy is straightforward: AI will displace employees, and so the revenues Compass earns from catering to workers across a range of industries will come under pressure.

Chart 2 – Compass Group and Sodexo SA – 12 months performance

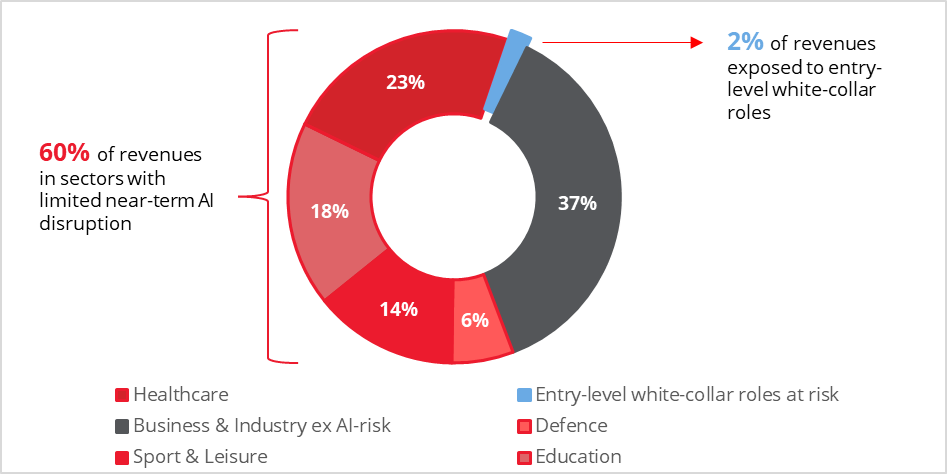

But when we look at who Compass actually feeds, the picture is more nuanced. As at September 2025, around 23% of revenues came from healthcare, 18% from education, 14% from sport and leisure and 6% from defence — some 60% of the group in aggregate – see Chart 3. It seems unlikely that AI will stop people falling ill, replace sports people or encourage us to cease education, and this part of the business also retains significant runway for growth, with around 40% of US hospitals and colleges still self-operating their catering.

Business & Industry represents about 39% of group revenues, but only part of that is directly exposed to the areas of white-collar employment most often cited as vulnerable to AI . Of that exposure, our analysis suggests that the group revenue tied to entry-level roles most at risk of displacement is, for now, a maximum of around 2% of sales. Oxford Economics supports our analysis in broader labour market terms: adoption is mainstream but still shallow, only around 10% of information-sector firms report AI replacing worker tasks, and its baseline scenario remains more labour-augmenting than labour-displacing .

This does not mean there is no risk. It does mean the risk appears manageable, likely to emerge over time through slower hiring rather than a sudden hit to revenues, and far smaller than the market reaction has implied.

Chart 3 – Compass Group revenue mix by end-market

When controversy knocks down the share price of a high‑return business, our job is not to predict the future with precision, but to calibrate the range of possible cash‑flow outcomes and ask whether the odds have shifted in our favour. In Compass’ case, the answer was clear.

At the lows in March and April, Compass was trading on a free cash flow yield of around 5%. At that valuation, the shares implied a markedly more pessimistic future than the company’s long-term record would suggest.

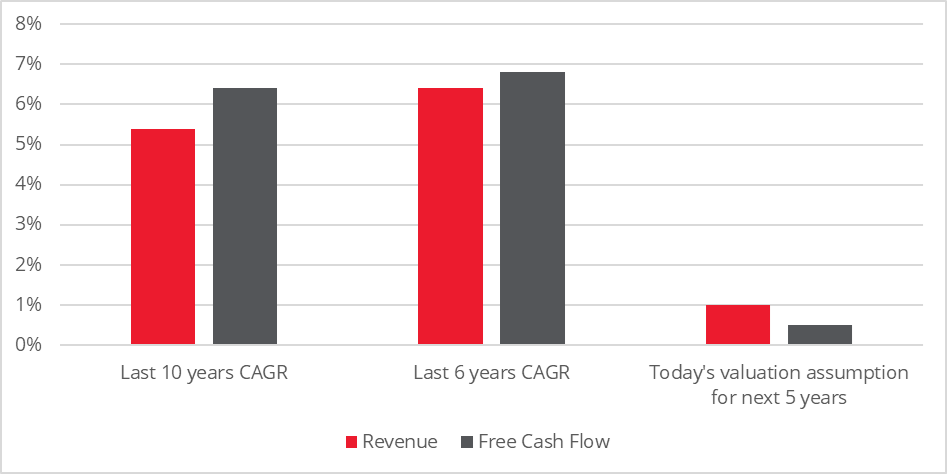

Even if one assumes that, over the next five years, Compass can grow revenues by only 1% per annum and free cash flow by less than 0.5%, followed by a 2% terminal growth rate, the shares would still only just decline from those levels, with the downside largely the time value of money. That compares with compound annual growth of more than 5% in both revenue and free cash flow over the last decade – see Chart 4.

In other words, the valuation at the March low was already pricing in an abrupt halt in Compass’s business. Those are the risk-reward metrics we seek out: situations where the asymmetry is skewed in our favour, rather than investing in richly valued stocks where continued AI-led, US exceptionalism is demanded.

Chart 4 – Compass historic revenue and free cash flow growth vs implied market assumptions

Compass is an excellent example of how the Global Equity Income Strategy is designed to exploit controversy to its advantage. The sell‑off in catering names, driven by AI and related fears, pushed Compass, a best-in-class company, into the team’s yield universe for the first time in years. This is because every holding must yield at least 25% more than the MSCI World Index at purchase. That yield discipline forces patience and avoids overpaying for certainty, momentum or the market’s current favourites.

From there, the key question is whether the controversy is likely to be temporary or permanent. By fishing in the same buckets of controversy time after time, the team builds a knowledge library of repeating patterns, helping us to judge whether a problem is an opportunity or something to avoid. For Compass, the evidence suggests the market has extrapolated a narrow risk too broadly across the business in a way that fails to reflect its highly diversified sector exposure and the limited share of revenues tied directly to at‑risk roles.

Finally, the team tests whether company cash flows can suffer downturn. With Compass, the breadth of end‑markets, and a long record of growing revenues and free cash flow through past cycles all point to a business capable of withstanding the shock that recent headlines have imagined.

In an AI‑driven market regime, first‑order thinking tends to dominate: “AI will write code, so software companies are dead”, or “AI will automate offices, so anything feeding office workers is uninvestable”. Compass Group shows why that can be a costly simplification, given its diversified end‑markets, modest direct exposure to at‑risk roles and history of compounding cash flows.

The Global Equity Income team’s process is deliberately built to thrive when this kind of extrapolation meets valuation reality. In that sense, Compass is not just a stock we own; it is a case study in how to invest through AI‑driven disruption. By focusing on what can be measured – cash flows, contract structures, end‑market exposures and starting valuations – controversy can become a potential source of long‑term income and capital growth.

Sources

[1] See ‘A return to normality’, Redwheel, March 2026

[2] This security has been selected to highlight the strategy’s investment methodology and is not representative of the strategy’s performance. The investment strategy holds a broad range of securities. Portfolio holdings are subject to change at any time without notice. This information should not be construed as a recommendation to purchase or sell any security

[3] Bloomberg, May 2026: ‘StanChart joins AI push with cuts to ‘lower-value human capital’’

[4] Oxford Economics, A primer on the AI boom, May 2026

[5] Bloomberg, May 2026, company financials and Redwheel analysis

Key Information

No investment strategy or risk management technique can guarantee returns or eliminate risks in any market environment. Past performance is not a guide to the future. The prices of investments and income from them may fall as well as rise and investors may not get back the full amount invested. Forecasts and estimates are based upon subjective assumptions about circumstances and events that may not yet have taken place and may never do so. The statements and opinions expressed in this article are those of the author as of the date of publication, and do not necessarily represent the view of Redwheel. This article does not constitute investment advice and the information shown is for illustrative purposes only.

John Teahan, Portfolio Manager and Company Engagement Lead with the Redwheel Value and Income team, explores how virtual‑only AGM formats risk diluting public accountability, particularly for long‑term and retail investors. He argues that well‑designed hybrid AGMs can reconcile safety and convenience with the discipline and visibility of a physical meeting.

The Redwheel Emerging and Frontier Markets team explores what is driving this quiet bull market – from reform momentum and rerating potential to deeper structural supports – and asks how durable it might be.

Shaul Rosten, Analyst, Redwheel Value & Income, draws on Dietrich Bonhoeffer’s ‘Theory of Stupidity’, the recent Palantir–Burry spat and the rise of AI trading tools to show why rational, long-term investors still have a structural edge.

Redwheel ® and Ecofin ® are registered trademarks of RWC Partners Limited (“RWC”). The term “Redwheel” may include any one or more Redwheel branded regulated entities including RWC Asset Management LLP, which is authorised and regulated by the UK Financial Conduct Authority and the US Securities and Exchange Commission (“SEC”); RWC Asset Advisors (US) LLC, which is registered with the SEC; RWC Singapore (Pte) Limited, which is licensed as a Licensed Fund Management Company by the Monetary Authority of Singapore; Redwheel Australia Pty Ltd is an Australian Financial Services Licensee with the Australian Securities and Investment Commission; and Redwheel Europe Fondsmæglerselskab A/S which is regulated by the Danish Financial Supervisory Authority.

Redwheel may act as investment manager or adviser, or otherwise provide services, to more than one product pursuing a similar investment strategy or focus to the product detailed in this document. Redwheel and RWC (together “Redwheel Group”) seeks to minimise any conflicts of interest, and endeavours to act at all times in accordance with its legal and regulatory obligations as well as its own policies and codes of conduct.

This document is directed only at professional, institutional, wholesale or qualified investors. The services provided by Redwheel are available only to such persons. It is not intended for distribution to and should not be relied on by any person who would qualify as a retail or individual investor in any jurisdiction or for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to local law or regulation.

This document has been prepared for general information purposes only and has not been delivered for registration in any jurisdiction nor has its content been reviewed or approved by any regulatory authority in any jurisdiction.

The information contained herein does not constitute: (i) a binding legal agreement; (ii) legal, regulatory, tax, accounting or other advice; (iii) an offer, recommendation or solicitation to buy or sell shares in any fund, security, commodity, financial instrument or derivative linked to, or otherwise included in a portfolio managed or advised by Redwheel; or (iv) an offer to enter into any other transaction whatsoever (each a “Transaction”). Redwheel Group bears no responsibility for your investment research and/or investment decisions and you should consult your own lawyer, accountant, tax adviser or other professional adviser before entering into any Transaction. No representations and/or warranties are made that the information contained herein is either up to date and/or accurate and is not intended to be used or relied upon by any counterparty, investor or any other third party.

Redwheel Group uses information from third party vendors, such as statistical and other data, that it believes to be reliable. However, the accuracy of this data, which may be used to calculate results or otherwise compile data that finds its way over time into Redwheel Group research data stored on its systems, is not guaranteed. If such information is not accurate, some of the conclusions reached or statements made may be adversely affected. Any opinion expressed herein, which may be subjective in nature, may not be shared by all directors, officers, employees, or representatives of Group and may be subject to change without notice. Redwheel Group is not liable for any decisions made or actions or inactions taken by you or others based on the contents of this document and neither Redwheel Group nor any of its directors, officers, employees, or representatives (including affiliates) accepts any liability whatsoever for any errors and/or omissions or for any direct, indirect, special, incidental, or consequential loss, damages, or expenses of any kind howsoever arising from the use of, or reliance on, any information contained herein.

Information contained in this document should not be viewed as indicative of future results. Past performance of any Transaction is not indicative of future results. The value of investments can go down as well as up. Certain assumptions and forward looking statements may have been made either for modelling purposes, to simplify the presentation and/or calculation of any projections or estimates contained herein and Redwheel Group does not represent that that any such assumptions or statements will reflect actual future events or that all assumptions have been considered or stated. There can be no assurance that estimated returns or projections will be realised or that actual returns or performance results will not materially differ from those estimated herein. Some of the information contained in this document may be aggregated data of Transactions executed by Redwheel that has been compiled so as not to identify the underlying Transactions of any particular customer.

No representations or warranties of any kind are intended or should be inferred with respect to the economic return from, or the tax consequences of, an investment in a Redwheel-managed fund.

This document expresses no views as to the suitability or appropriateness of the fund or any other investments described herein to the individual circumstances of any recipient.

The information transmitted is intended only for the person or entity to which it has been given and may contain confidential and/or privileged material. In accepting receipt of the information transmitted you agree that you and/or your affiliates, partners, directors, officers and employees, as applicable, will keep all information strictly confidential. Any review, retransmission, dissemination or other use of, or taking of any action in reliance upon, this information is prohibited. Any distribution or reproduction of this document is not authorised and is prohibited without the express written consent of Redwheel Group.

Funds managed by Redwheel are not, and will not be, registered under the Securities Act of 1933 (the “Securities Act”) and are not available for purchase by US persons (as defined in Regulation S under the Securities Act) except to persons who are “qualified purchasers” (as defined in the Investment Company Act of 1940) and “accredited investors” (as defined in Rule 501(a) under the Securities Act).

This document does not constitute an offer to sell, purchase, subscribe for or otherwise invest in units or shares of any fund managed by Redwheel. Any offering is made only pursuant to the relevant offering document and the relevant subscription application. Prospective investors should review the offering memorandum in its entirety, including the risk factors in the offering memorandum, before making a decision to invest.

AIFMD and Distribution in the European Economic Area (“EEA”)

The Alternative Fund Managers Directive (Directive 2011/61/EU) (“AIFMD”) is a regulatory regime which came into full effect in the EEA on 22 July 2014. RWC Asset Management LLP is an Alternative Investment Fund Manager (an “AIFM”) to certain funds managed by it (each an “AIF”). The AIFM is required to make available to investors certain prescribed information prior to their investment in an AIF. The majority of the prescribed information is contained in the latest Offering Document of the AIF. The remainder of the prescribed information is contained in the relevant AIF’s annual report and accounts. All of the information is provided in accordance with the AIFMD.

In relation to each member state of the EEA (each a “Member State”), this document may only be distributed and shares in a Redwheel fund (“Shares”) may only be offered and placed to the extent that (a) the relevant Redwheel fund is permitted to be marketed to professional investors in accordance with the AIFMD (as implemented into the local law/regulation of the relevant Member State); or (b) this document may otherwise be lawfully distributed and the Shares may lawfully be offered or placed in that Member State (including at the initiative of the investor).

Information Required for Offering in Switzerland of Foreign Collective Investment Schemes to Qualified Investors within the meaning of Article 10 CISA.

This is an advertising document.

The representative and paying agent of the Redwheel-managed funds in Switzerland (the “Representative in Switzerland”) FIRST INDEPENDENT FUND SERVICES LTD, Feldeggstrasse 12, CH-8008 Zurich. Swiss Paying Agent: Helvetische Bank AG, Seefeldstrasse 215, CH-8008 Zurich. In respect of the units of the Redwheel-managed funds offered in Switzerland, the place of performance is at the registered office of the Swiss Representative. The place of jurisdiction is at the registered office of the Swiss Representative or at the registered office or place of residence of the investor.

Redwheel ® and Ecofin ® are registered trademarks of RWC Partners Limited. The term “Redwheel” may include any one or more Redwheel regulated entities including RWC Asset Management LLP, which is authorised and regulated by the Financial Conduct Authority in the United Kingdom (“RWC”). RWC is incorporated in England and Wales with its registered office at Verde 4th Floor, 10 Bressenden Place, London, SW1E 5DH, United Kingdom and its registered number is OC332015.

No investment strategy or risk management technique can guarantee returns or eliminate risks in any market environment.The term “RWC” may include any one or more RWC branded entities including RWC Partners Limited and RWC Asset Management LLP, each of which is authorised and regulated by the UK Financial Conduct Authority and, in the case of RWC Asset Management LLP, the US Securities and Exchange Commission; RWC Asset Advisors (US) LLC, which is registered with the US Securities and Exchange Commission; and RWC Singapore (Pte) Limited, which is licensed as a Licensed Fund Management Company by the Monetary Authority of Singapore.RWC may act as investment manager or adviser, or otherwise provide services, to more than one product pursuing a similar investment strategy or focus to the product detailed in this audio. RWC seeks to minimise any conflicts of interest, and endeavours to act at all times in accordance with its legal and regulatory obligations as well as its own policies and codes of conduct.This audio is directed only at professional, institutional, wholesale or qualified investors. The services provided by RWC are available only to such persons. It is not intended for distribution to and should not be relied on by any person who would qualify as a retail or individual investor in any jurisdiction or for distribution to, or use by, any person or entity in any jurisdiction where such distribution or use would be contrary to local law or regulation.This audio has been prepared for general information purposes only and has not been delivered for registration in any jurisdiction nor has its content been reviewed or approved by any regulatory authority in any jurisdiction. The information contained herein does not constitute: (i) a binding legal agreement; (ii) legal, regulatory, tax, accounting or other advice; (iii) an offer, recommendation or solicitation to buy or sell shares in any fund, security, commodity, financial instrument or derivative linked to, or otherwise included in a portfolio managed or advised by RWC; or(iv) an offer to enter into any other transaction whatsoever (each a “Transaction”). No representations and/or warranties are made that the information contained herein is either up to date and/or accurate and is not intended to be used or relied upon by any counterparty, investor or any other third party.RWC uses information from third party vendors, such as statistical and other data, that it believes to be reliable. However, the accuracy of this data, which may be used to calculate results or otherwise compile data that finds its way over time into RWC research data stored on its systems, is not guaranteed. If such information is not accurate, some of the conclusions reached or statements made may be adversely affected. RWC bears no responsibility for your investment research and/or investment decisions and you should consult your own lawyer, accountant, tax adviser or other professional adviser before entering into any Transaction. Any opinion expressed herein, which may be subjective in nature, may not be shared by all directors, officers, employees, or representatives of RWC and may be subject to change without notice. RWC is not liable for any decisions made or actions or in actions taken by you or others based on the contents of this audio and neither RWC nor any of its directors, officers, employees, or representatives (including affiliates) accepts any liability whatsoever for any errors and/or omissions or for any direct, indirect, special, incidental, or consequential loss, damages, or expenses of any kind howsoever arising from the use of, or reliance on, any information contained herein.Information contained in this audio should not be viewed as indicative of future results. Past performance of any Transaction is not indicative of future results. The value of investments can go down as well as up. Certain assumptions and forward looking statements may have been made either for modelling purposes, to simplify the audio and/or calculation of any projections or estimates contained herein and RWC does not represent that that any such assumptions or statements will reflect actual future events or that all assumptions have been considered or stated. Forward-looking statements are inherently uncertain, and changing factors such as those affecting the markets generally, or those affecting particular industries or issuers, may cause results to differ from those discussed. Accordingly, there can be no assurance that estimated returns or projections will be realised or that actual returns or performance results will not materially differ from those estimated herein. Some of the information contained in this audio may be aggregated data of Transactions executed by RWC that has been compiled so as not to identify the underlying Transactions of any particular customer.The information transmitted is intended only for the person or entity to which it has been given and may contain confidential and/or privileged material. In accepting receipt of the information transmitted you agree that you and/or your affiliates, partners, directors, officers and employees, as applicable, will keep all information strictly confidential. Any review, retransmission, dissemination or other use of, or taking of any action in reliance upon, this information is prohibited. The information contained herein is confidential and is intended for the exclusive use of the intended recipient(s) to which this audio has been provided. Any distribution or reproduction of this audio is not authorised and is prohibited without the express written consent of RWC or any of its affiliates.Changes in rates of exchange may cause the value of such investments to fluctuate. An investor may not be able to get back the amount invested and the loss on realisation may be very high and could result in a substantial or complete loss of the investment. In addition, an investor who realises their investment in a RWC-managed fund after a short period may not realise the amount originally invested as a result of charges made on the issue and/or redemption of such investment. The value of such interests for the purposes of purchases may differ from their value for the purpose of redemptions. No representations or warranties of any kind are intended or should be inferred with respect to the economic return from, or the tax consequences of, an investment in a RWC-managed fund. Current tax levels and reliefs may change. Depending on individual circumstances, this may affect investment returns. Nothing in this document constitutes advice on the merits of buying or selling a particular investment. This audio expresses no views as to the suitability or appropriateness of the fund or any other investments described herein to the individual circumstances of any recipient.AIFMD and Distribution in the European Economic Area (“EEA”)The Alternative Fund Managers Directive (Directive 2011/61/EU)(“AIFMD”) is a regulatory regime which came into full effect in the EEA on 22 July 2014. RWC Asset Management LLP is an Alternative Investment Fund Manager (an “AIFM”) to certain funds managed by it (each an “AIF”). The AIFM is required to make available to investors certain prescribed information prior to their investment in an AIF. The majority of the prescribed information is contained in the latest Offering Document of the AIF. The remainder of the prescribed information is contained in the relevant AIF’s annual report and accounts. All of the information is provided in accordance with the AIFMD.In relation to each member state of the EEA (each a “Member State”),this document may only be distributed and shares in a RWC fund(“Shares”) may only be offered and placed to the extent that (a) the relevant RWC fund is permitted to be marketed to professional investors in accordance with the AIFMD (as implemented into the local law/regulation of the relevant Member State); or (b) this audio may otherwise be lawfully distributed and the Shares may lawfully offered or placed in that Member State (including at the initiative of the investor).Information Required for Distribution of Foreign Collective Investment Schemes to Qualified Investors in SwitzerlandThe representative and paying agent of the RWC-managed funds in Switzerland (the “Representative in Switzerland”) FIRST INDEPENDENT FUND SERVICES LTD, Klausstrasse 33, CH-8008 Zurich. Swiss Paying Agent: Helvetische Bank AG, Seefeldstrasse 215, CH-8008 Zurich. In respect of the units of the RWC-managed funds distributed in Switzerland, the place of performance and jurisdiction is at the registered office of the Representative in Switzerland.