The manufacturing winners of the last 20 years such as China and Korea look set to be challenged by the next generation of emerging markets (NGEN). We believe that countries such as Vietnam, Indonesia and Romania are on track to contest the world’s production hubs over the next two decades, driven by powerful secular tailwinds.

NGEN look set to be on a well-trodden path to economic success

Successful economic development is a well-trodden path. Since the Industrial Revolution of the late 18th Century, many countries have achieved economic success driven by young, educated workforces which go on to attract investment into their burgeoning, manufacturing-led industries. The Far East’s economic miracle over the last 50 years is the world’s latest example of this powerful secular pathway.

Populations have tended to migrate away from agrarian employment to focus on factory and office work. As a result, urbanisation levels have increased dramatically with a positive impact on consumption. The most potent example of this has been the transformation of China since the 1980s from a relatively low-income country to the second largest economy in the world.

Since 2010, the world has generally reverted to an historically normalised, moderate growth environment with stable trade and investment penetration ratios. Even a ‘flat’ world in terms of overall trade and investment penetration still leaves ample room for new EM economies to jump on the bandwagon and rise through the ranks of the export value-added chain in our opinion.

We believe that the historically proven development path towards labour-intensive, manufacturing export-led growth will benefit economies such as Vietnam, Hungary and Mexico. They are poised to potentially benefit from the same economic tailwinds that Korea, Taiwan and China experienced over the last few decades.

A new economic cycle focused on tangible asset investment

The period since the Global Financial Crisis (GFC) saw greater investment in innovation and intangible assets than in previous business cycles, enabled by an environment of low input cost prices, low inflation and a low cost of capital.

However, since the launch of our Next Generation Emerging Markets Equity strategy five years ago, we have held the view that the world has entered a new economic cycle characterised by increased tangible capex. Investor priorities appear to be shifting towards the physical world, driving increased spending in areas such as renewable energy and the relocation of global manufacturing.

In previous cycles, countries such as China, Korea and Taiwan were among the beneficiaries. This time around, thanks to the success of these countries in industries such as semiconductors and the internet, we believe that smaller emerging economies will be the key beneficiaries of increased tangible asset capex.

COVID-19 accelerated supply chain diversification away from China, and the Russian invasion of Ukraine highlighted just how fragile the world’s energy infrastructure had become. The world continues to need to restructure its supply chains to reduce over-reliance on China, which now accounts for 28% of world manufacturing activity.[1] We believe that this development will lead to a similar capex cycle to the one we saw in the early 2000s.

The significance of such a structural shift cannot be underestimated as both the current and the capital accounts of NGEN economies would likely benefit. This would in turn attract foreign direct investment (FDI) and portfolio investments comparable to Japan in the 1950s and 60s, and China in the 2000s. Given such structural tailwinds, we believe that the surpluses on NGEN external accounts would likely be sustained and would be supportive for their respective currencies and equity markets.

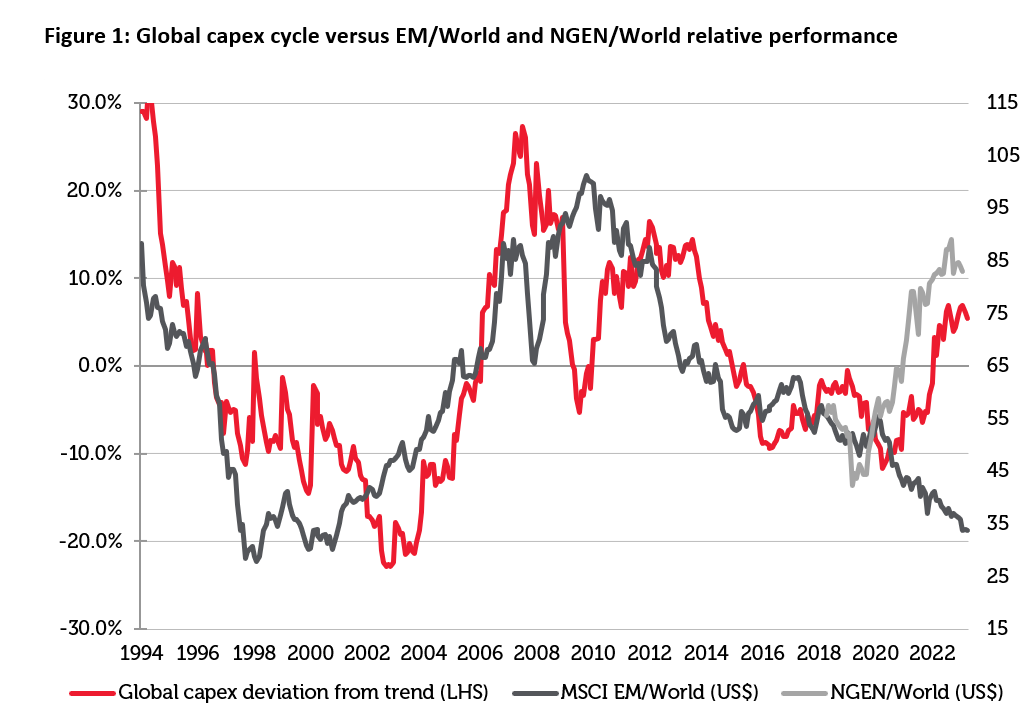

Looking at the chart below, we are already seeing NGEN stock markets benefit as global capex increases.

Source: Redwheel, CLSA, Factset, Datastream – Refinitiv as at 31 March 2024. The information shown above is for illustrative purposes. Past performance is not a guide to future results. EM refers to the MSCI Emerging Market Index, World refers to the MSCI World Index and NGEN refers to the Redwheel Next Generation Emerging Market Fund.

Industrial leadership changes over time. The first generation of successful new products often gives way to improved versions by different manufacturers. For example, popular mobile phone manufacturers at the beginning of the cellular telephony age ceded market share to producers of smartphones in the 2000s. Similarly, the automotive industry is undergoing change with the combustion engine being replaced by electric vehicles. The dominant producers of electric vehicles, at least in terms of volume, are likely to be Chinese. Electric vehicle (EV) producers in China are scaling up their manufacturing to cement market leadership globally in this new technology. Gaining scale allows costs to be reduced, vehicles to be produced more cheaply and accelerates dominance of the mass market.

The NGEN Opportunity

Despite the attractive returns delivered to date, we believe that the valuations in NGEN markets remain attractive, trading at significant discounts to the majority of their larger emerging market counterparts.

Current volatility in global stock markets, driven by concerns over Federal Reserve policy normalisation or global geopolitical uncertainty, present a timely opportunity to invest in select NGEN economies as they progress along their long-term structural growth trajectories. We believe that the correlation of these markets with broader global indices is low as their fortunes are largely tied to their own economic fundamentals.

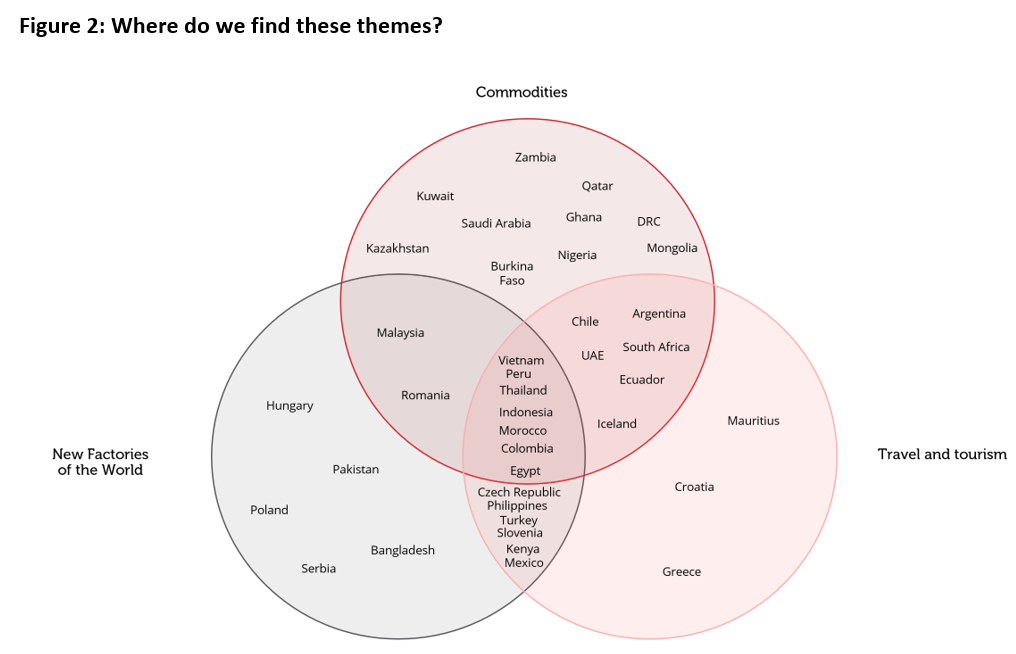

With several decades of investment experience in EM behind them, the team has identified three key structural drivers of growth: New Factories of the World, Travel and Tourism and Commodities. We anticipate that these themes will be the growth drivers for NGEN economies going forward. History rhymes if it does not always repeat.

Source: Redwheel, as at 30 April 2024. The information shown above is for illustrative purposes.

‘Travel and Tourism’ account for roughly 12% of world GDP and 1 out of 10 jobs globally are linked to travel.[2] As disposable incomes have risen over the last few decades, tourism levels have increased dramatically worldwide and we expect this structural trend to continue. The Covid-19 pandemic interrupted this trend but as the world has re-opened its borders, travel and tourism continue to recover. Emerging and frontier economies tend to benefit considerably as tourist arrivals increase in countries such as Turkey, Thailand, UAE and Greece.

The ‘New Factories of the World’ theme includes countries with low-cost labour and cheap manufacturing capacity that attract capital in search of higher returns. The world is now diversifying away from its manufacturing reliance on China for political and strategic reasons. Companies are looking to new economies in which to expand their production centres for the next two decades. Chinese firms themselves are often at the forefront of FDI into these new manufacturing locations as they also need to remain cost-competitive on the international stage.

One example of this transition is the Korean electronics giant Samsung which moved a large portion of its electronics manufacturing to Vietnam over the last decade from both Korea and China. In Hungary, we have recently seen the largest Chinese EV manufacturer, BYD announce plans to build a new manufacturing plant, making it the first Chinese car maker to build a passenger car plant in the EU.[3] Another example is Tesla’s announcement to build their new factory in Nuevo León in the north of Mexico. The US $5 billion investment will create 6,000 jobs and is the largest single investment in Mexico.[4]

And lastly, ‘Commodities’ look attractive in our view. Investing to achieve net zero emission targets, relocation of manufacturing capacity, increasing defence spending or building data centres for generative AI applications are all activities consuming significant amounts of materials and energy.

The supply of materials such as copper, uranium and aluminium that are crucial in these sectors remains constrained after a decade of under-investment. New mines and resources are predominantly being discovered across Africa and South America but costs of production have increased dramatically alongside greater ESG requirements for cleaner extractive methods.

The Russian invasion of Ukraine served to highlight the fragility of the world’s supply of energy, food and minerals. With limited spending into exploration and production, this fragile supply picture is likely to persist for many years.

The key potential beneficiaries of this are those NGEN economies that are net exporters of hard and soft commodities: Peru and Chile for copper and other base metals, Indonesia and Thailand for metals and soft commodities in addition to Colombia and the Gulf States for oil and gas.

Our investment thesis remains intact

The five years since our strategy was launched is just the beginning of the time-honoured journey that NGEN economies must take towards economic development. Nevertheless, it represents an important milestone for a strategy focusing exclusively on markets that have taken significant strides towards economic success and are already benefiting from multiple secular tailwinds.

Sources:

[1] Safeguard Global, as at September 2023

[2] WorldBank, as at 30th April 2024

[3] Financial Times, as at December 2023

Key Information

No investment strategy or risk management technique can guarantee returns or eliminate risks in any market environment. Past performance is not a guide to future results. The prices of investments and income from them may fall as well as rise and an investor’s investment is subject to potential loss, in whole or in part. Forecasts and estimates are based upon subjective assumptions about circumstances and events that may not yet have taken place and may never do so. The statements and opinions expressed in this article are those of the author as of the date of publication, and do not necessarily represent the view of Redwheel. This article does not constitute investment advice and the information shown is for illustrative purposes only.