It ain’t over until it’s over

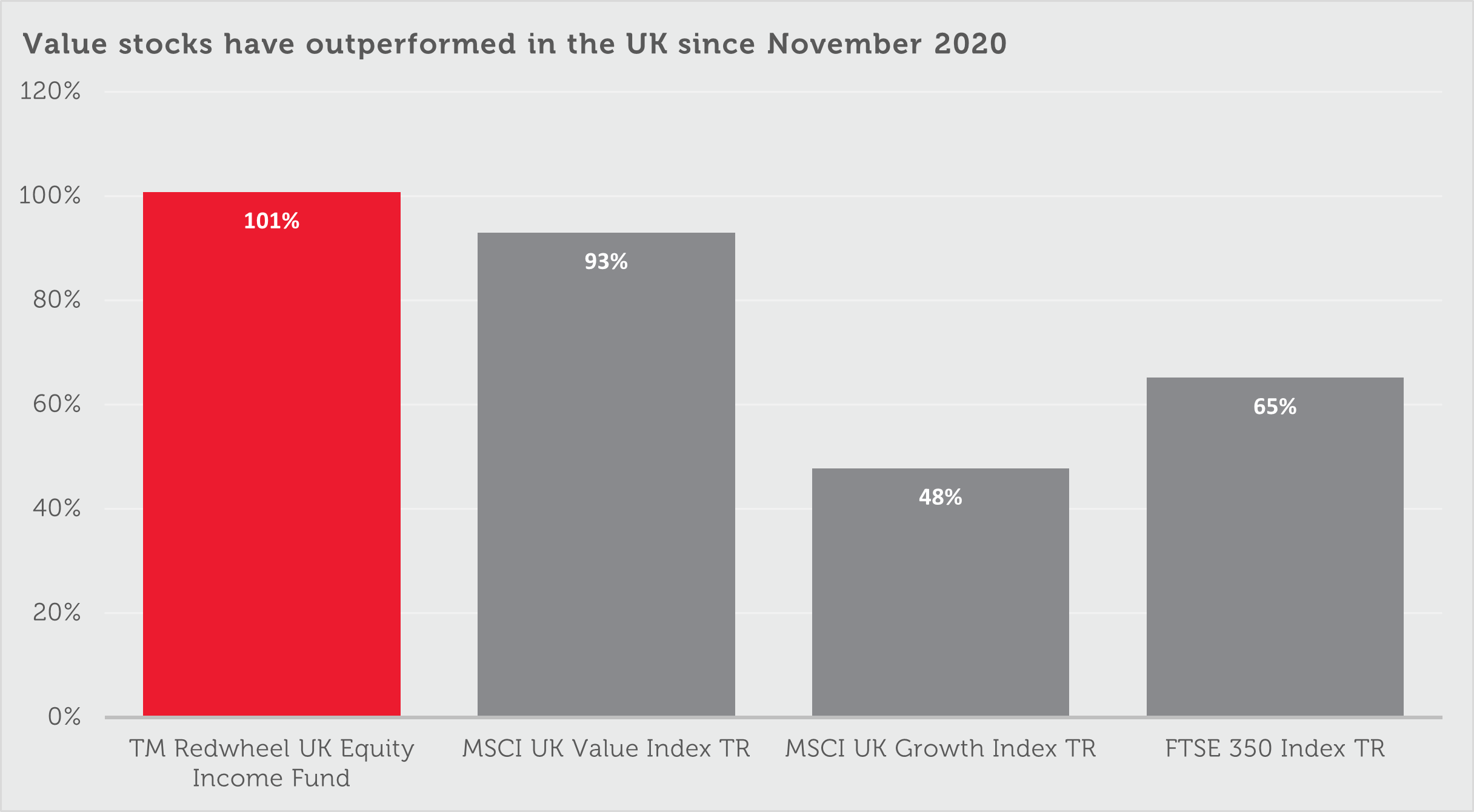

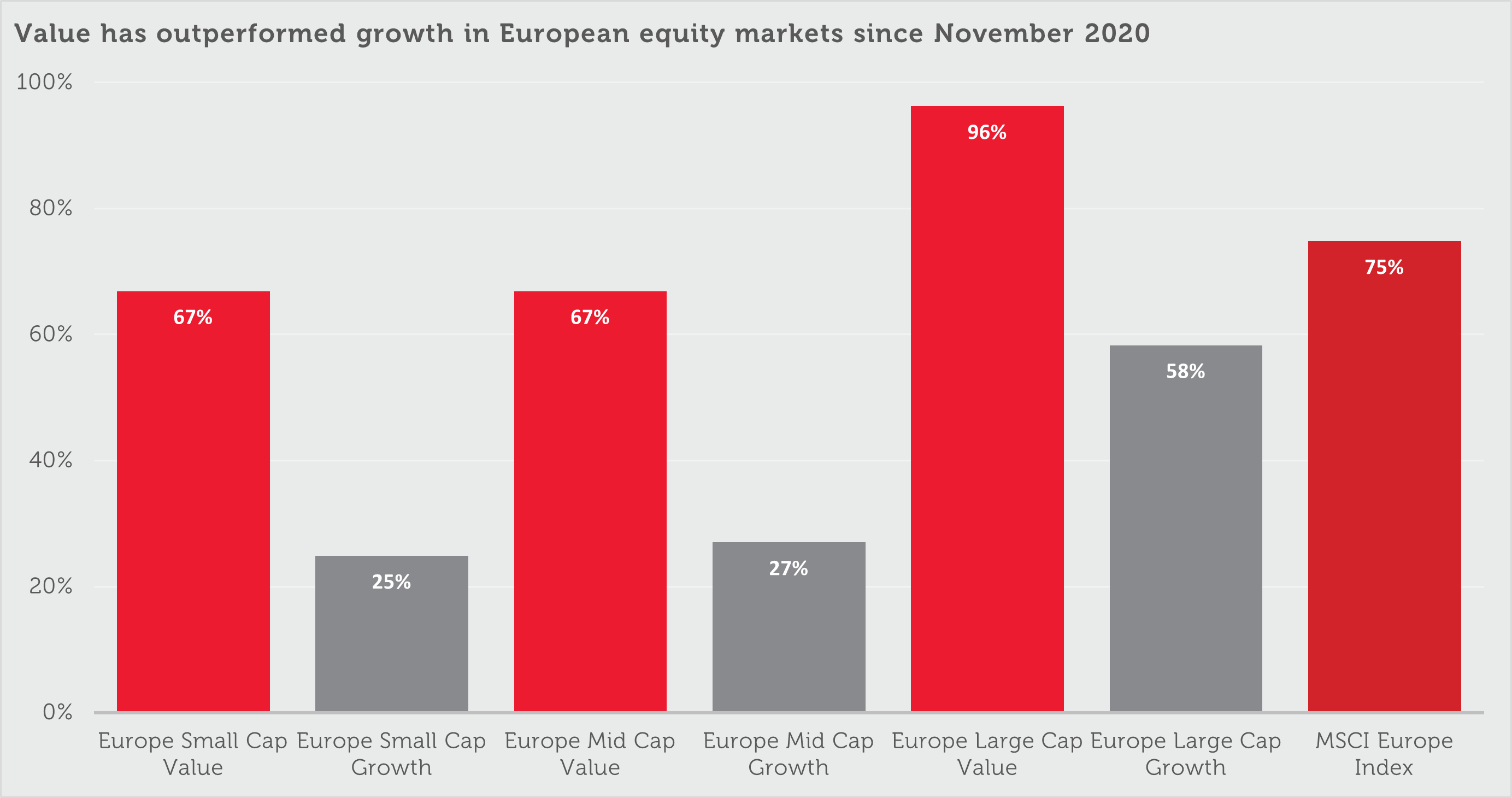

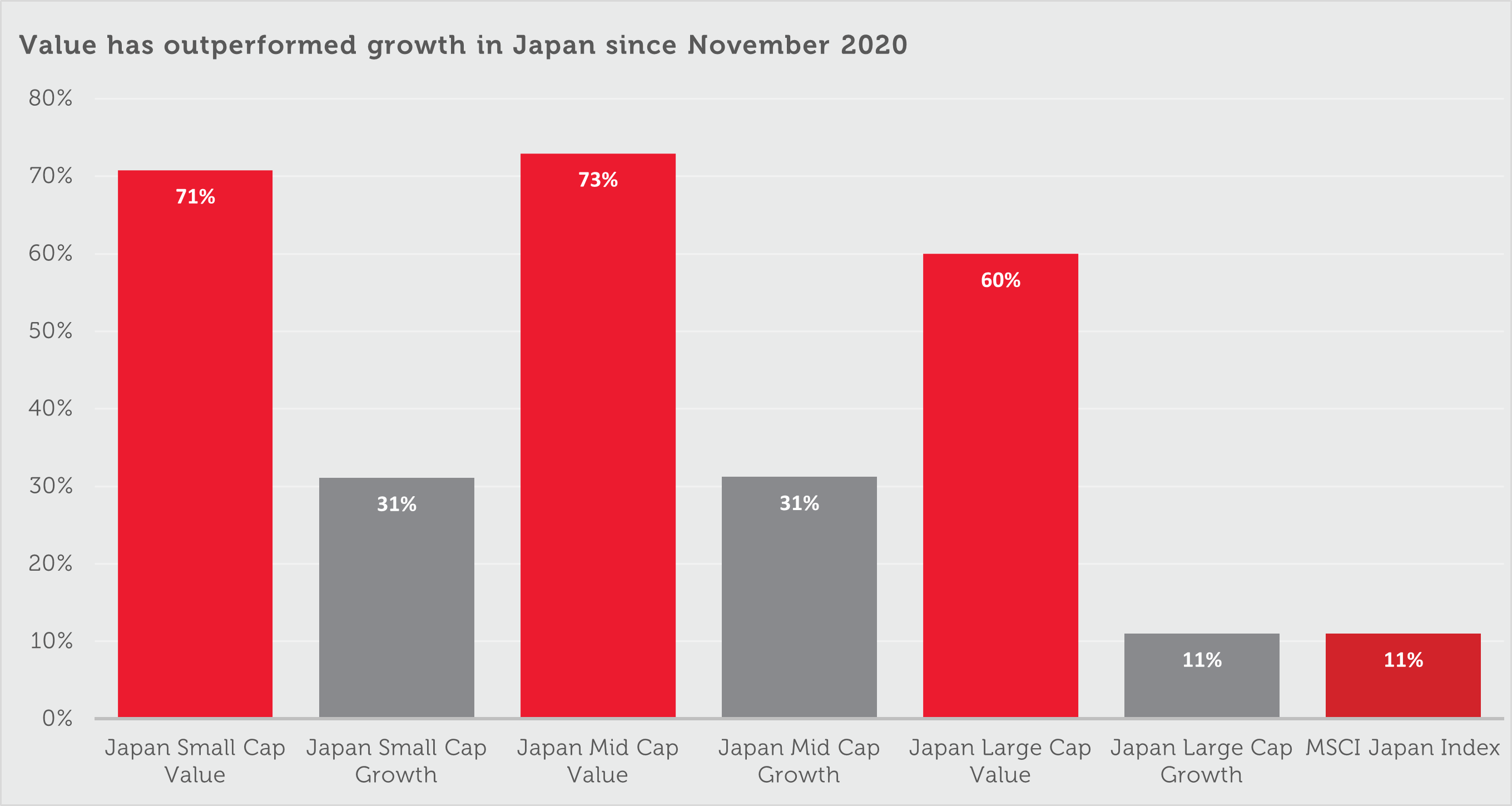

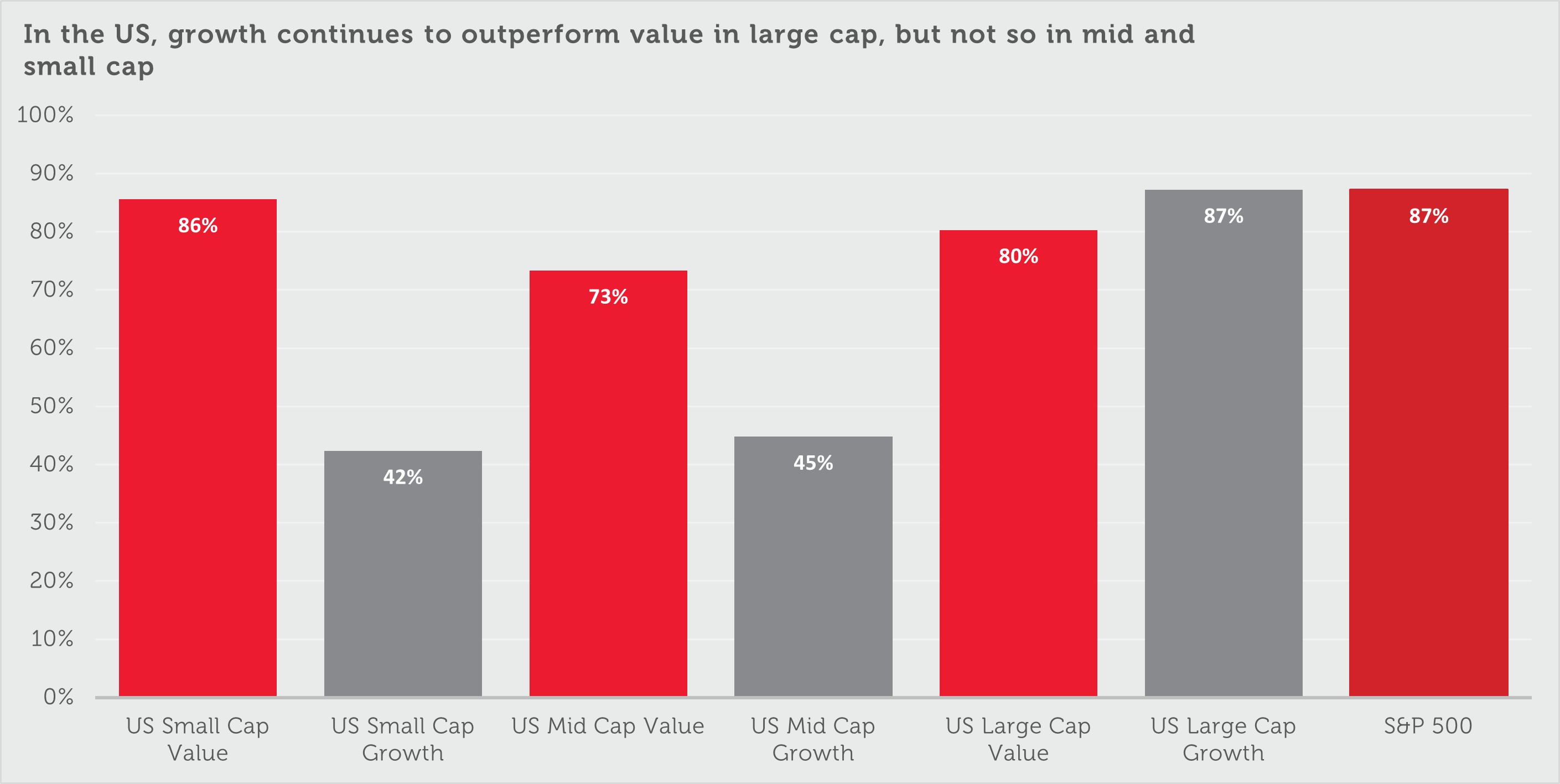

The long-term empirical evidence behind the concept of value investing is robust. Lowly valued stocks have outperformed in every complete decade of the last 100 years, with one exception – the 2010s. From this perspective, it is not surprising to see value reasserting itself, almost everywhere, over the last few years [1].

Indeed, the market’s continued infatuation with a handful of US technology stocks may be described as “the last shoe to drop” as far as the growth obsession of the 2010s is concerned. Everywhere else, value has resumed its former dominance.

The value renaissance has been good news for TM Redwheel UK Equity Income Fund holders, and we are confident that this will continue. We are, and always will be, disciplined value investors, and the excesses that accumulated in the era of low interest rates and quantitative easing will take a very long time to unwind. We believe this should represent a tailwind for value investors that lasts many years into the future.

In other words, there remains plenty for value investors to look forward to.